The article below is an excerpt from our Q4 2024 commentary.

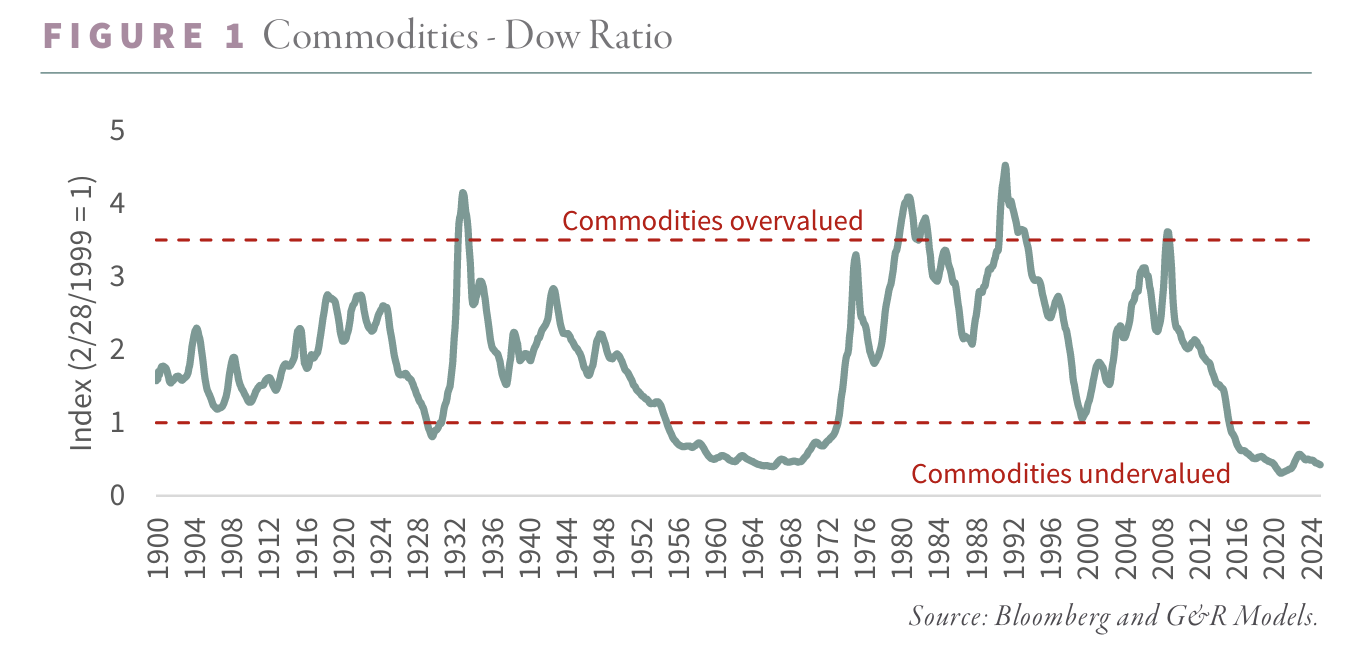

We believe the time to buy natural resource equities has arrived. History, with its characteristic flair for the dramatic, has shown that commodity markets do not simply meander— they surge and collapse in sweeping, decade-spanning cycles. Prices can climb tenfold in a matter of years, only to later crumble, resetting the stage for the next act. Time and again, we have published a particular chart that tracks the ratio of commodity prices to stocks, using the Dow Jones Industrial Average as its benchmark. Barring the brief, COVID-induced plunge, commodities are now as undervalued relative to stocks as they have ever been. And now, fresh research suggests that the tide is about to turn—that the long-dormant natural resource bull market may be stirring once again.

Two recent developments have prompted us to revisit this pressing subject. The first is a series of remarks—subtle but unmistakable—by members of the Trump Administration, hinting at what some have dubbed the “Mar-a-Lago Accords.” If these hints amount to more than mere rhetoric, we could be standing at the threshold of a major shift in the monetary regime. And history, in its usual unsentimental fashion, reminds us that every commodity bear cycle has met its end with precisely such a shock. We see no reason to believe this time will be any different.

If we are correct, a major shift in the global monetary system may be imminent. History offers a clear precedent: every past commodity bull market has been set in motion by a similar regime change. The policies now being proposed—whether intended or not—are likely to produce the same effect, triggering another surge in commodities and natural resource equities. Investors would do well to take heed and position their portfolios accordingly before such an event materializes.

The second development is the striking impression left on us by "The Rise of Carry," a book by Lee, Lee, and Coldiron. The authors dissect so-called “carry regimes,” periods defined by suppressed volatility and an abundance of leverage. While their analysis does not explicitly address natural resource markets, we could not help but draw a connection. The long, dramatic cycles of commodities appear inextricably linked to these broader “carry regime” cycles. If our intuition is correct, then natural resource equities may prove to be one of the few asset classes capable of shielding investors from the eventual unwinding of today’s great carry trade.

Over the past 125 years, commodities have endured four episodes of extreme undervaluation relative to equities. The first three concluded in 1929, 1969, and 1999—each marking the start of an era in which commodities and natural resource equities dramatically outpaced the broader market.

The fourth such period began in 2011, hitting a double bottom—first in 2016 and again amid the COVID turmoil of 2020. Notably, despite a strong recovery since then, we have yet to witness the full force of the next great commodity bull market. But the signs are gathering, the pattern is familiar, and we believe an inflection point is near.

History offers a blueprint: each prolonged phase of commodity weakness has followed the same arc. A boom begins, first drawing in capital, then fueling a surge in production. Supply inevitably overtakes demand, and prices, once euphoric, collapse—shedding 75% or more in absolute terms. What follows is a period of radical undervaluation, setting the stage for the next great reversal. We have seen this before, and we suspect we are seeing it again.

The first three episodes of radical commodity undervaluation all proved to be extraordinary entry points for buyers of natural resource equities—counterintuitive as that may have seemed at the time. Even amid the stock market crash of 1929 and the ensuing Great Depression, a basket of commodity stocks purchased at the market’s peak that summer would have doubled in value by 1940, while the S&P 500 languished at half its former high. Between 1968 and 1980, a similar portfolio of resource equities multiplied fivefold, leaving the S&P 500’s mere doubling in the dust. Natural resource stocks not only outpaced inflation but delivered positive real returns while the broader equity market suffered an inflation-adjusted loss. From 1999 to 2011, history repeated itself: commodity equities once again surged, far outstripping the S&P 500.

Each of these periods of commodity undervaluation coincided with a speculative frenzy occurring elsewhere in the market, typically centered on emerging technology. The 1920s bull market belonged to radio stocks, with Radio Corporation of America (RCA) rising an astonishing 300-fold, from $1.50 in 1920 to $505 by 1929. In the 1960s, it was semiconductors, with Fairchild Camera and Instrument—the progenitor of Fairchild Semiconductor and Intel—soaring from $20 to $200 a share. The late 1990s saw the dot-com boom, epitomized by Cisco Systems, which skyrocketed nearly 1,200-fold, compounding at more than 100% annually between 1990 and 2000. Most recently, the Magnificent Seven have dominated, with Nvidia leading the charge—its stock climbing nearly 500-fold since 2013.

History is nothing if not repetitive, and past commodity bear markets have consistently coincided with market manias centered around so-called “one decision” stocks—securities whose appeal rested on a single, overly simplistic investment rationale. These were the stocks investors could supposedly buy and hold forever, immune to valuation concerns and economic cycles, at least until reality intruded.

The “Roaring Twenties” provided the first example: a broad and exuberant rally in which nearly any investment strategy worked—except, of course, buying natural resource equities. The 1960s saw the rise of the conglomerate boom, in which high-multiple companies used their richly valued stock as currency to acquire lower-multiple firms. Financial sleight of hand manufactured earnings growth, driving valuations even higher in a self-reinforcing spiral--until the spell broke. Later, the “Nifty Fifty,” a collection of blue-chip growth stocks that investors purchased on faith alone, regardless of price, became the quintessential “one decision stocks”-once you bought them, you never had to sell.

The 1990s, of course, belonged to the dot-com bubble. Simply appending “.com” to a company’s name could send its stock soaring, while analysts spun elaborate justifications for valuing firms with no revenue as if they were the next General Electric. Most recently, the dominant narrative has centered on the hyperscalers, the tech giants that have captured a disproportionate share of market gains. Meanwhile, the investment landscape has tilted sharply away from active management toward passive ETFs, a shift that has further amplified the concentration of capital in a handful of mega-cap stocks.

Each prolonged period of commodity underperformance has unfolded against a backdrop of exceptionally loose credit conditions. In the latter half of the 1920s, the United States embarked on its first experiment with quantitative easing. Benjamin Strong, then Governor of the Federal Reserve Bank of New York, expanded the Fed’s balance sheet—not to support the domestic economy, which was thriving, but to shore up the struggling British pound, still burdened by the inflation and debts of World War I.

The 1960s saw a different form of excess. The U.S. government ran persistent deficits, attempting to finance both the Vietnam War and an ambitious domestic social spending agenda without imposing fiscal discipline. The 1990s, in turn, were dominated by the so-called “Greenspan Put,” a period in which Federal Reserve Chairman Alan Greenspan maintained an aggressively accommodative monetary stance even in the face of a robust economy.

Following the Global Financial Crisis, the Federal Reserve’s interventions escalated further. A series of quantitative easing programs saw the Fed’s balance sheet swell from $900 billion in 2007 to $9 trillion by 2022—a scale of monetary expansion without historical precedent.

During each of these episodes, easy money propelled the equity market to levels that would have been otherwise unattainable. Surging valuations, fueled by abundant liquidity, funneled vast sums of capital into the fastest-growing sectors of the market while draining investment from real assets, commodities, and natural resource equities. The result was a steady erosion of these sectors’ market weightings. Between 1926 and 1929, the share of energy and materials stocks in the U.S. market fell by half, from 22% to 11%. The same pattern played out in the postwar boom, as their weight dropped from 29% in 1957 to 14% by 1970. From 1980—a peak moment for resource equities—their weighting collapsed from 34% to under 5% by 2000. The most recent cycle followed suit: from their 2008 highs to the depths of the COVID-driven selloff in 2020, energy and materials declined from 17% of the S&P 500 to an all-time low of just 2.1%. While they have since recovered somewhat, their presence in the market remains marginal at a mere 3.4%.

Historically, every commodity bear market has ended with an unforeseen shift in the global monetary order. These so-called “Black Swan” events served as the necessary mechanism to correct the growing distortions in the global financial system and reprice real assets. Each of these shifts was invariably followed by a significant devaluation of the U.S. dollar relative to gold.

The commodity bear market of the 1920s came to its inevitable conclusion when the classical gold standard was abandoned. During World War I, most European nations had suspended the gold backing of their currencies to finance the war effort, setting in motion a monetary distortion that would take more than a decade to resolve. After the Versailles Treaty in 1919, many of these countries made strained attempts to restore their currencies to prewar gold parity, with Britain leading the charge. As Chancellor of the Exchequer, Winston Churchill spearheaded a series of painful deflationary policies to strengthen the pound—a decision he would later call the greatest regret of his career. John Maynard Keynes, for his part, loudly objected, but his warnings went unheeded.

Meanwhile, across the Atlantic, Federal Reserve Governor Benjamin Strong sought to prop up the British currency by weakening the dollar, expanding the Fed’s balance sheet in the first real experiment with U.S. monetary interventionism. Yet the effort ultimately failed. Strong’s sudden death in 1928 led to the swift reversal of his policies, tightening credit conditions just as market imbalances were peaking—an abrupt shift that would contribute to the onset of the Great Depression. By 1929, the classical gold standard, which had governed the international monetary system since the end of the Napoleonic Wars, was effectively dead. In 1932, Franklin Roosevelt took matters into his own hands, outlawing private ownership of gold in the U.S. before promptly devaluing the dollar by 40%, raising the official gold price from $20.67 to $35 per ounce.

The next great commodity bear market, in the 1960s, ended with the collapse of the Bretton Woods system. In the aftermath of World War II, the United States had orchestrated a new international monetary framework, pegging the dollar to gold at $35 per ounce, with other currencies in turn pegged to the dollar. This arrangement held for two decades, but by the late 1960s, persistent U.S. deficit spending—driven by both the Vietnam War and ambitious domestic programs—led foreign governments to increasingly exchange their dollars for gold. The pressure intensified in 1968, forcing President Lyndon Johnson to intervene. He attempted to stem the outflows by urging Congress to repeal the legal requirement that the dollar be backed by at least 25% gold reserves. Instead of stabilizing the system, the move only reinforced expectations of devaluation, causing the international gold price to rise further. By 1971, with the system on the brink of collapse, President Nixon delivered the final shock: closing the gold window and ending the dollar’s convertibility into gold. Bretton Woods was no more, and over the next decade, the dollar’s value relative to gold would collapse by 95%.

The 1990s saw a period of breakneck growth across East Asia, driven by export booms and surging capital inflows. Many of these economies maintained fixed exchange rates against the U.S. dollar, a strategy that worked well so long as foreign capital continued pouring in. The implicit understanding was that, in the event of sudden capital flight, the U.S. and the International Monetary Fund (IMF) would step in with dollar swap lines to maintain stability. That understanding was put to the test in July 1997, when Thailand, unable to defend its currency, abandoned its dollar peg. The decision triggered a violent unwinding of speculative capital from emerging market currencies. Despite earlier assurances, the U.S. and the IMF withheld support, and the resulting contagion sent shockwaves through global markets. Within six months, the Thai baht had collapsed by 58%, while the Indonesian rupiah fell by 85% between 1997 and 1998.

The crisis forced a painful but necessary adjustment. Emerging market economies, unable to count on outside intervention, revalued their currencies at much lower levels to regain export competitiveness and repair their trade balances. The results were dramatic: Thailand’s current account deficit, which stood at 8% of GDP in 1996, swung to a 12.5% surplus by 1998. This marked the beginning of a new global monetary order, one that economic historian Russell Napier later dubbed the “No Name Regime.” Under this system—still in place today—the U.S. runs persistent and sizable trade deficits, while surplus nations accumulate dollars and recycle them into Treasury bonds, fueling ever-rising U.S. debt and deficits.

In the 25 years following the crisis, foreign and international investors increased their holdings of U.S. Treasuries by $7.5 trillion. Meanwhile, gold, long a barometer of confidence in monetary regimes—surged eightfold between 1999 and 2011, reflecting an effective 86% devaluation of the dollar against gold.

We have long maintained that the current period of commodity undervaluation would ultimately conclude with a fundamental shift in the global monetary order. Until recently, we expected this shift to originate from the BRIC nations. China, in particular, has spearheaded efforts to move away from the dollar in bilateral trade settlement, gradually reducing its reliance on the U.S. currency. By last year, nearly 10% of all international trade had already moved outside the dollar-based system—a quiet but unmistakable sign of change.

More recently, however, our thinking has evolved. Rather than de-dollarization being driven externally, we now believe the catalyst may emerge from within the United States itself. Instead of retreating from the dollar’s role as the global reserve currency, policymakers appear poised to double down on it, introducing a series of sweeping reforms that the media has begun referring to as the “Mar-a-Lago Accords.” Though details remain scarce, both Treasury Secretary Bessent and proposed Council of Economic Advisors Chairman Miran have offered hints as to their likely structure. In short, the reforms are expected to include revaluing the Federal Reserve’s gold holdings, restructuring portions of the national debt, and implementing a tariff regime designed to define what Miran describes as a “global commonwealth” of allied nations. Whether these measures will succeed remains an open question, but there is no doubt they represent a fundamental break from the existing global monetary framework.

At our Investor Day in New York this past October, we had the opportunity to interview Neil Howe, author of "The Fourth Turning." Howe’s thesis outlines an 80-to-100-year cycle in American history, in which institutional structures are periodically dismantled and rebuilt in response to profound crises. He argues that we are currently in the midst of one such turning, the last having reached its climax during World War II. Within this framework, President Trump, Secretary Bessent, and Miran emerge as figures not of continuity, but of radical institutional transformation and disruption.

Historically, similar changes have ushered in a period of commodity outperformance relative to the broader market.

But this is not merely a concern for commodity investors. As we reflected on "The Rise of Carry," it became evident that the commodity bear market is only one facet of a much broader cycle—the carry regime. The authors illustrate how carry bubbles permeate every asset class, creating a false sense of diversification. In reality, most investors have unwittingly doubled down on their exposure to carry trades, leaving them dangerously vulnerable to an unwind. The most recent instance came in 2022, when the S&P 500, the Bloomberg U.S. Bond Index, and the Bloomberg All Hedge Fund Index all declined between 6% and 28%, illustrating how deeply entrenched the carry trade had become.

For true protection against a carry unwind, investors must actively seek exposure to areas outside the carry regime. The events of 2022 provide a useful case study. While most asset classes suffered, energy stocks in the S&P 500 surged 65% even as the broader index plunged nearly 20%. The lesson is clear: when the cycle turns, capital flows shift dramatically, and those positioned correctly stand to benefit.

What exactly is a carry regime? The authors of "The Rise of Carry" begin with its most classic example: borrowing in a low-interest-rate currency—typically the Japanese yen— and investing in a higher-yielding economy, such as Australia. As long as the yen does not appreciate too aggressively against the Australian dollar, the investor earns a positive “carry” return—the difference between the cost of borrowing and the yield on the investment. Studies have shown that hedging future currency risk can create what appears to be a persistent arbitrage.

However, Lee, Lee, and Coldiron make a crucial observation: many investments not traditionally considered carry trades share the same fundamental characteristics and function in much the same way. They broaden the definition of a carry trade to encompass any investment that relies on leverage and is structurally short volatility. The underlying principle is simple: as long as initial conditions hold—specifically, that volatility remains low—the investment delivers a steady, positive expected return. In the case of the classic yen-Australia carry, the trade is profitable so long as the exchange rate remains within expectations. If tomorrow looks like today, the bet pays off.

But herein lies the danger. During extended periods of low volatility, capital floods into these trades, amplifying the perceived arbitrage and pushing asset prices higher. The more money that piles in, the greater the eventual mispricing, and the more precarious the rally becomes. Given the highly leveraged nature of these trades, the unwinding of the bubble is often violent. Traders have long referred to carry trades as akin to “picking up pennies in front of a steamroller”—a strategy that delivers steady, modest returns so long as conditions remain stable, but one that collapses catastrophically the moment volatility reappears.

Any large, leveraged short-volatility bubble produces a series of highly predictable outcomes. First, the sheer volume of capital chasing short-volatility strategies suppresses volatility itself. The more investors pile in, the more yesterday’s trade continues to work today, creating a self-reinforcing cycle. Capital floods into momentum strategies, rewarding size over value. Large-cap equities, which attract the most inflows, outperform smaller companies. Value investing, which depends on the eventual recognition of mispricings, lags behind growth investing, which thrives on investors extrapolating recent success far into the future. Risk premiums compress as volatility remains subdued, driving yields across asset classes toward historically low levels. As equity risk premiums erode, asset prices surge, fueling an unprecedented hyper-financialization. The stock market’s capitalization expands at a rate far outpacing the underlying economy. This unique market structure—one where leverage, compressed risk premiums, and capital concentration define the investment landscape—is what the authors refer to as a “carry regime.”

Lee, Lee, and Coldiron focus on the most recent carry regime, which took hold in the aftermath of the Global Financial Crisis. Since the S&P 500 bottomed in March 2009, it has delivered an extraordinary 16.3% compounded annual growth rate (CAGR)—nearly three times the 5.7% CAGR observed between 1927 and 2009. Volatility was systematically suppressed, with the standard deviation of monthly returns running nearly 25% lower than in the prior 82 years. Equity valuations expanded, driving earnings yields lower, while the spread between the Case-Shiller P/E ratio and the risk-free rate collapsed by 82%, from 7.3% to just 1.2%, as yields across asset classes converged.

In such an environment, “buying the dip” became more than just a trading strategy—it became dogma. The short-volatility trade proved remarkably profitable, interrupted only briefly by the “vol-mageddon” shock of 2018. And like all carry regimes, this one relied on ample leverage. By 2020, negative-yielding debt had ballooned to $18 trillion. Equity margin loans, a direct measure of market leverage, swelled from $120 billion in 2009 to $500 billion by 2021. The conditions were textbook: a low-volatility, high-leverage boom that, like its predecessors, was bound to eventually hit its breaking point.

Carry regimes create a powerful feedback loop, continuously attracting more capital into the trade and allowing it to expand well beyond fundamental limits. The end result has been an unprecedented hyper-financialization, in which U.S. public equity markets have swelled to over 200% of GDP—the highest level in history.

As capital flooded into carry trades, equity returns became increasingly concentrated among the largest winners. Cheap financing and suppressed volatility rewarded success with even more success, pushing the strongest stocks even higher. The result: the largest 10% of stocks by capitalization now account for a staggering 75% of the total market—the highest level of concentration in a century.

Momentum strategies thrived, diverting capital away from active management and into passive strategies. As the market’s biggest stocks continued their relentless rise, they became increasingly dominant in capitalization-weighted indices, further entrenching their position. This, in turn, made it more difficult for active managers to outperform, reinforcing the appeal of passive investing. The cycle fed on itself: passive strategies’ outperformance attracted even greater inflows, keeping the momentum trade alive. Trillions of dollars that once flowed into actively managed mutual funds were instead funneled into passive ETFs, further accelerating the shift and deepening the concentration of market leadership.

A carry regime will continue to expand as long as it appears to be working, regardless of underlying fundamentals. Because it diverts capital in a way that ignores fundamental value, it inevitably misprices risk and distorts capital allocation. These distortions create structural imbalances. One of the most notable is that the combination of cheap capital and suppressed volatility leads investors to assign higher valuations to long-dated and uncertain cash flows. As a result, in contrast to historical norms, carry regimes tend to see growth stocks outperform value stocks. High-multiple, high-growth, long-duration assets benefit disproportionately, while tangible assets—commodities and natural resource equities—are left starved of capital.

As capital flees, the performance of commodity and natural resource stocks deteriorates, reinforcing their neglect. Momentum strategies exacerbate the trend, driving these stocks lower still. Hedge funds, spotting an easy trade, pile in on the short side. With few natural buyers remaining, prices plunge.

The proliferation of alternative investments—most notably hedge funds and private equity— is both a symptom and an accelerant of a carry regime. Hedge funds are key agents of the system because of their compensation structure: managers collect a percentage of investment gains but are not similarly penalized for losses. This asymmetry incentivizes short-volatility strategies. As long as tomorrow looks like today, they capture supernormal profits without the expectation of repaying them when the inevitable shock arrives. The failure of Long-Term Capital Management in 1998 remains the quintessential example of how hedge funds gravitate toward, and further reinforce, the leveraged short-volatility mindset.

Private equity funds are even more direct participants in carry regimes. Their entire business model depends on borrowing vast sums of cheap debt to acquire companies. As long as the cost of capital remains low and market conditions remain stable, they can generate above-market returns, extracting enormous fees in the process. So long as the cycle persists, the rewards are immense—but, like all carry trades, the strategy relies on a world that does not change.

Rather than providing diversification, many alternative investments actually deepen an investor’s exposure to the carry regime. During a carry unwind—most recently experienced in 2022—these supposedly uncorrelated assets often fall in tandem, revealing their hidden linkages. What was once thought to be a hedge turns out to be merely another expression of the same trade.

Natural resource equities, by contrast, largely exist outside the carry regime. Unlike long-duration, high-growth assets, they do not attract massive capital inflows during periods of suppressed volatility and cheap financing. Once they begin underperforming, they take on the characteristics least desirable in a carry regime: value and negative momentum. As a result, they are systematically starved of capital. However, when the cycle turns, their detachment from the prevailing financial regime can become a rare advantage. During the 2022 carry unwind, energy was one of only two sectors that posted gains, soaring 65% while the broader S&P 500 plunged.

Lee, Lee, and Coldiron devote most of "The Rise of Carry" to analyzing the present market cycle, only briefly touching on past regimes. Yet our research indicates that previous periods of extreme commodity undervaluation—the late 1920s, the 1960s, and the 1990s—were all accompanied by major carry bubbles. The historical pattern is clear: each era of financial excess, driven by leverage and suppressed volatility, has eventually met its reckoning, and each reckoning has marked the turning point for commodities.

We identified four distinct carry regimes, each followed by a severe unwind. The first unfolded between January 1927 and August 1929, ending in the brutal downturn that lasted until June 1932. The second began in July 1962 and persisted until November 1968, with its unwind extending until September 1974. The third emerged in November 1990, lasting through August 2000, before collapsing in a selloff that dragged on until September 2002. The most recent carry regime commenced in March 2009 and remains ongoing. Looking back over nearly a century of market history, we found that carry regimes have dominated 35% of the time, unwinds 11%, and non-carry markets—the periods in between—accounted for the remaining 54%.

A striking pattern emerged: prior carry regimes bore a strong resemblance to today’s market dynamics.

On average, the S&P 500 delivered superior returns during carry regimes, rising 1.4% per month compared with 0.8% during non-carry periods. However, unwinds were brutal, with the index falling an average of 2% per month.

Value investing, traditionally a stalwart over long time horizons, saw its edge shrink considerably in carry regimes. According to Professor French’s historical dataset, the value factor outperformed by 43 basis points per month during non-carry periods but by a mere 8 basis points per month during carry regimes. When carry trades unwound, value significantly outperformed, as high-multiple growth stocks collapsed.

The same trend held for small-cap equities. They outperformed by 31 basis points per month in non-carry periods but saw that advantage shrink to just 11 basis points during carry regimes. When unwinds struck, small-cap stocks underperformed by 21 basis points per month, likely due to a wave of bankruptcies among the most leveraged firms.

Yields consistently compressed during past carry regimes. The average spread between equity earnings yields and Treasury rates fell to just 2.4%, compared with 6.0% in non-carry periods, as investors bid up asset prices while risk premiums eroded.

Momentum, by contrast, flourished in carry regimes. It returned 1.27% per month during these periods, compared with only 0.48% in non-carry environments, as capital continued chasing prior winners.

Hyper-financialization was another hallmark of carry regimes. U.S. equity market capitalization surged to an average of 120% of GDP during these periods, compared with just 58% in non-carry environments.

Volatility suppression was widespread. Large drawdowns of greater than 10% in the S&P 500 were milder and recovered more quickly during carry regimes, averaging a 17% decline with a rebound in 339 days. By contrast, non-carry periods saw an average drawdown of 25%, requiring 817 days for recovery.

Most notably, every past carry regime culminated in a massive mispricing of risk, followed by a violent unwind that inflicted deep losses on investors. And in every instance, the cycle’s collapse coincided with the start of a period of sustained natural resource outperformance, lasting years.

Carry regimes have a way of sustaining themselves—until they don’t. They function like a well-oiled machine, running smoothly and predictably, drawing in ever more capital, reinforcing the same trades, and compounding imbalances. The cycle builds upon itself, accelerating distortions until the sheer weight of misallocation begins to strain the very infrastructure of the global financial system. At some point, the pressure becomes too great, and the system is forced into a dramatic shift. This moment—the breaking point—marks the beginning of the carry unwind.

Carry regimes thrive on continuity. As long as tomorrow looks like today, the trade holds, leverage builds, and returns accumulate. But when the global monetary order shifts, tomorrow looks radically different. Suddenly, the foundation that supported years of steady, low-volatility gains crumbles, forcing a violent unwinding of leveraged positions.

History has made this pattern clear. Every prior carry unwind has aligned with a fundamental transformation in the monetary system. The collapse of the classical gold standard in 1929, the unraveling of Bretton Woods in 1968, and the forced realignment of emerging market currency pegs in 1998 all served as catalysts. Each marked the end of an era of artificial stability—and the beginning of a carry unwind.

Recent remarks from President Trump, Treasury Secretary Bessent, and Miran suggest that we may be nearing another such moment of reckoning. Each has, in their own way, pointed to the mounting distortions in the current monetary system and the growing imbalances that threaten its stability. Bessent, in particular, has been explicit about the need to address the financial system’s underlying “plumbing” as a means of restoring equilibrium—an acknowledgment that the present framework is not merely strained but unsustainable.

Taken together, these signals leave little doubt: a significant shift in the global monetary order is not only possible but increasingly at the forefront of the administration’s agenda. The precise form this change will take remains uncertain, but history tells us that when policymakers begin openly questioning the status quo, the status quo is already on borrowed time.

Though still in its early stages, the rumored framework for what the media has dubbed the Mar-a-Lago Accords is beginning to take shape. Based on comments from Treasury Secretary Bessent, the emerging plan appears to center on reorganizing global trade and financial relationships into distinct tiers, with countries sorted according to their currency policies, trade agreements, and security alliances. Under this system, nations deemed “friendly” would enjoy tariff-free access to the U.S. market and broad access to U.S. dollar liquidity lines. Tariffs, rather than being strictly punitive, would function as a form of economic demarcation—determining whether a given country is inside the bloc, on its periphery, or entirely outside.

Another key component of the rumored plan involves restructuring U.S. Treasury debt. There has been speculation about issuing 50-year nonmarketable Treasury bonds, which would not trade freely but could be sold back to the U.S. government or pledged as collateral—presumably at par—against repo loans in times of financial distress. It is not difficult to imagine that participation in this system could eventually become a prerequisite for inclusion in the new trading bloc itself.

Perhaps the most consequential element under discussion is the potential revaluation of the Federal Reserve’s gold holdings. Owing to legislation dating back to President Roosevelt’s gold confiscation order, the Fed was compelled in 1934 to surrender its gold to the Treasury in exchange for a paper IOU. This asset has remained on the Fed’s balance sheet at a fixed price of $42 per ounce since 1973—a stark contrast to gold’s current market price of $2,900 per ounce. With a simple majority in Congress, the Federal Reserve could revalue these holdings, instantly increasing its balance sheet assets by roughly $800 billion. This unrealized capital gain would flow to the Fed’s equity account—better known as the Treasury General Account—creating an immediate $800 billion liquidity injection without requiring commercial bank intermediation. Such a maneuver could also serve to offset the dollar strength that might accompany the widespread imposition of tariffs.

Though still speculative, the outlines of this proposed regime suggest a dramatic reordering of the global financial and trade system—one that would mark the most significant shift in U.S. monetary policy since the closure of the gold window in 1971.

Each of these proposed measures is designed to do one thing: reassert the dollar’s dominance as the undisputed global reserve currency. While the BRIC nations have been steadily pushing for de-dollarization, Bessent appears to be pursuing something far more ambitious—a sweeping “re-dollarization” that seeks to re-anchor the global financial system around the U.S. currency with an entirely new set of incentives.

Whether the administration’s efforts will succeed is impossible to say. But within our framework, the success or failure of any individual policy may be beside the point. What is certain is that the Mar-a-Lago Accords represent the most significant proposed shift in the global monetary system since the original Bretton Woods agreement in 1945. Bessent and Miran are speaking about the world’s financial “plumbing” in terms more radical than anything heard in decades, signaling that a major break from the status quo is being actively considered at the highest levels.

The world appears to be racing toward a fundamental shift in both the global monetary system and the geopolitical order. This is exactly the kind of moment that Neil Howe’s Fourth Turning framework would predict: a period of deep institutional upheaval that reshapes economic and political structures. For investors operating within the carry regime, the message is clear—tomorrow is unlikely to resemble yesterday. These are the moments in history that have coincided with the unwinding of massive financial imbalances. They are also the moments that have preceded long cycles of commodity and natural resource outperformance.

When will tomorrow arrive? If our intuition is correct, the administration is operating under severe time constraints. They likely need to clarify their plans by summer—before the political calendar takes over and the 2026 midterm elections begin to dominate the national conversation. That gives them weeks—maybe months—to set the stage.

For the first time since we began analyzing commodity cycles, a major catalyst appears to be emerging in the near term.

History tells us that these transitions—every one of them—have been marked by a devaluation of the dollar relative to gold. And if gold is the canary in the coal mine, it is singing loudly. The metal has surged 35% year over year and is already up 11% year-to-date. Perhaps, in its quiet and unambiguous way, gold is signaling that we are fast approaching the turning point.

Investors would do well to take notice. The assets that thrived under the carry regime are unlikely to perform in the next phase. True diversification—real diversification—will be essential. Natural resource equities, after a strong three-year run, have been mixed in recent months. But if history is any guide, this may be the final great buying opportunity before the carry regime unravels and commodities enter their next era of outperformance.

Curious to learn more? Read more in our Q4 2024 research newsletter, available for download below.

Registration with the SEC should not be construed as an endorsement or an indicator of investment skill, acumen or experience. Investments in securities are not insured, protected or guaranteed and may result in loss of income and/or principal. Historical performance is not indicative of any specific investment or future results. Investment process, strategies, philosophies, portfolio composition and allocations, security selection criteria and other parameters are current as of the date indicated and are subject to change without prior notice. This communication is distributed for informational purposes, and it is not to be construed as an offer, solicitation, recommendation, or endorsement of any particular security, products, or services. Nothing in this communication is intended to be or should be construed as individualized investment advice. All content is of a general nature and solely for educational, informational and illustrative purposes. This communication may include opinions and forward-looking statements. All statements other than statements of historical fact are opinions and/or forward-looking statements (including words such as “believe,” “estimate,” “anticipate,” “may,” “will,” “should,” and “expect”). Although we believe that the beliefs and expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such beliefs and expectations will prove to be correct. Various factors could cause actual results or performance to differ materially from those discussed in such forward-looking statements. All expressions of opinion are subject to change. You are cautioned not to place undue reliance on these forward-looking statements. Any dated information is published as of its date only. Dated and forward-looking statements speak only as of the date on which they are made. We undertake no obligation to update publicly or revise any dated or forward-looking statements. Any references to outside data, opinions or content are listed for informational purposes only and have not been independently verified for accuracy by the Adviser. Third-party views, opinions or forecasts do not necessarily reflect those of the Adviser or its employees. Unless stated otherwise, any mention of specific securities or investments is for illustrative purposes only. Adviser’s clients may or may not hold the securities discussed in their portfolios. Adviser makes no representations that any of the securities discussed have been or will be profitable. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio.