The article below is an excerpt from our Q2 2023 commentary.

Driven by concerns of an impending global recession, copper sentiment remained bearish during the second quarter. On the other hand, copper’s short-term fundamentals became increasingly bullish. Mine supply disappointed again in the first four months of 2023, according to the World Bureau of Metal Statistics (WBMS). Chilean production continues to be particularly problematic. For the first four months of the year, Chilean mine supply fell by nearly 2% compared to last year. Codelco warned that production could hit the lowest level in twenty-five years. In June, André Sougarret abruptly resigned as Codelco’s Chief Executive Officer after only one year on the job. Mr. Sougarret cited the numerous “complexities” facing the Chilean copper mines. Chile supplies almost one-quarter of all copper production and, in past letters, we have discussed the issues plaguing their copper industry; in particular, declining ore grades, water shortages, labor issues, and uncertain fiscal regimes all negatively impacted production. Unfortunately, we do not expect any of these issues to improve going forward. Global copper mine supply contracted by 0.2% in the first four months of 2023 compared to last year, driven by disappointments in Chile.

Meanwhile, global copper demand remained robust in both OECD and non-OECD countries. For the first four months of 2023, OECD copper demand increased by a robust 3.7%. Despite countless bearish articles in the financial press, Chinese copper demand continues to surge, with refined demand rising by 8% year-on-year. While China always dominates the headlines, we believe the pivotal element of Asian copper demand is India. We first wrote in 2018 that Indian copper demand was set to surge, very similar to China in 1999-2000. Even though few analysts have paid any attention, India’s copper consumption grew by almost 30% during the first four months of 2023 compared to last year. Global consumption in aggregate has surged 6% so far this year. Strong demand and weak mine supply continue to drive inventories to near all-time lows.

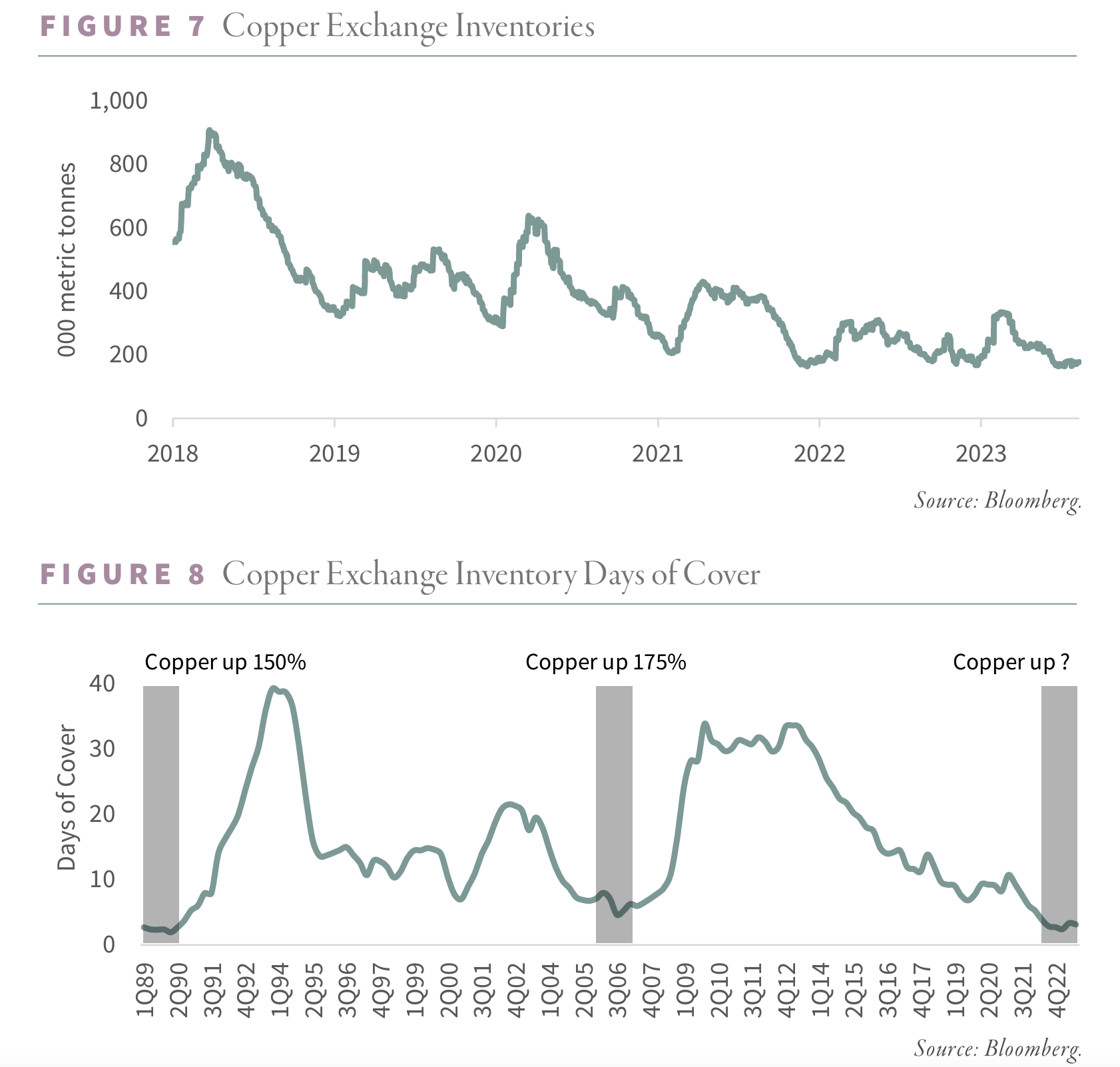

Exchange inventories on the Shanghai, London Metal Exchange (LME) and COMEX fell from a high of 900,000 tonnes reached in 2018 to only 170,000 tonnes today. Although inventories are twice as high as the all-time low of 75,000 tonnes reached in 2005, production has grown by nearly 60% over that time. As a result, when measured in days of consumption, exchange inventories are almost as low as in 2005.

Given the low exchange inventories and the bullish supply/demand trends, we believe speculators will soon panic much as they did back at the end of 2005 into 2006. Low inventories, combined with massive short covering, spiked copper prices higher by almost 200% in just six months. We are now potentially set up for a recurrence of that 2005-2006 copper price spike.

Although we remain concerned about the universally bullish outlook adopted by the global metal analytic and investment community—a topic discussed in last quarter’s letter—we believe the rapidly tightening underlying fundamentals will push copper prices significantly higher in the next six to twelve months. For those investors that have exited their copper investments on global recessionary fears, we believe the copper’s weakness in the second quarter has given investors another excellent opportunity to increase their exposure.

Intrigued? We invite you to download or revisit our entire Q2 2023 research letter, available below.

You may also listen to our roundtable discussion with Marko Papic, Parter & Chief Strategist of Clocktower Group (recorded in September 2023), "Russia's Role in Geopolitics: Navigating Natural Resource Investments in a Shifting Landscape."

Registration with the SEC should not be construed as an endorsement or an indicator of investment skill, acumen or experience. Investments in securities are not insured, protected or guaranteed and may result in loss of income and/or principal. Historical performance is not indicative of any specific investment or future results. Investment process, strategies, philosophies, portfolio composition and allocations, security selection criteria and other parameters are current as of the date indicated and are subject to change without prior notice. This communication is distributed for informational purposes, and it is not to be construed as an offer, solicitation, recommendation, or endorsement of any particular security, products, or services. Nothing in this communication is intended to be or should be construed as individualized investment advice. All content is of a general nature and solely for educational, informational and illustrative purposes. This communication may include opinions and forward-looking statements. All statements other than statements of historical fact are opinions and/or forward-looking statements (including words such as “believe,” “estimate,” “anticipate,” “may,” “will,” “should,” and “expect”). Although we believe that the beliefs and expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such beliefs and expectations will prove to be correct. Various factors could cause actual results or performance to differ materially from those discussed in such forward-looking statements. All expressions of opinion are subject to change. You are cautioned not to place undue reliance on these forward-looking statements. Any dated information is published as of its date only. Dated and forward-looking statements speak only as of the date on which they are made. We undertake no obligation to update publicly or revise any dated or forward-looking statements. Any references to outside data, opinions or content are listed for informational purposes only and have not been independently verified for accuracy by the Adviser. Third-party views, opinions or forecasts do not necessarily reflect those of the Adviser or its employees. Unless stated otherwise, any mention of specific securities or investments is for illustrative purposes only. Adviser’s clients may or may not hold the securities discussed in their portfolios. Adviser makes no representations that any of the securities discussed have been or will be profitable. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio.