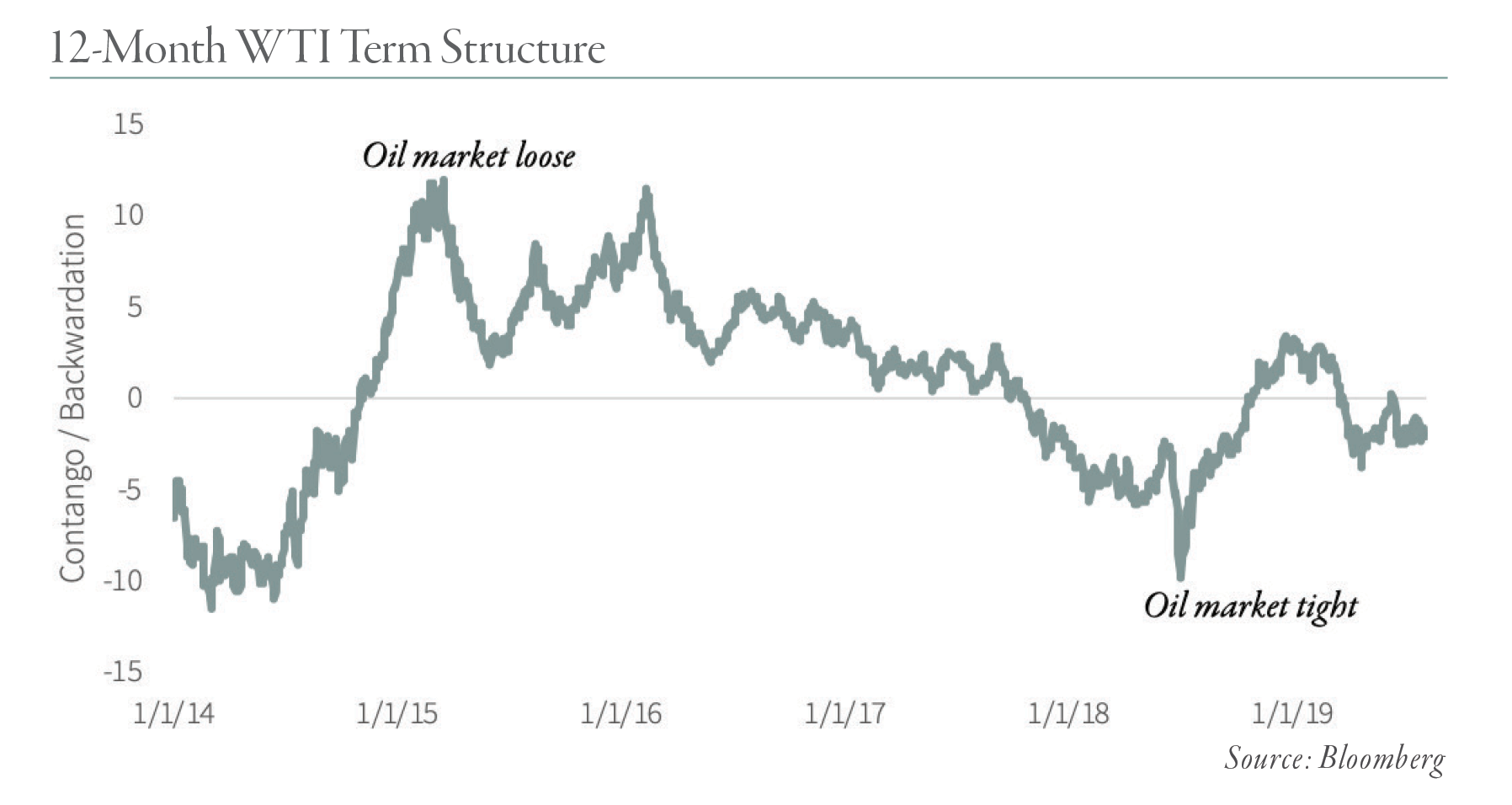

“While the conventional wisdom suggests the oil markets are in a sustained glut, the pronounced backwardization tells us that there is no truth in this belief.”

For nearly 30 years, we have been studying long, drawn-out bear markets. As we stated last week while discussing commodity prices relative to commodity stock prices, one of our observations has been that distinct anomalies develop at or near the bottom of these protracted periods of investor negativity.

As we discuss in the oil section of our most-recent letter, there is a widely held belief among investors that the oil markets are currently oversupplied. The fact that U.S. inventory behavior has been weak during the first half has only added to this bearish outlook. We believe that recent inventory behavior has been skewed by various short-term issues stemming largely from issues surrounding the US sanctions against Iran. Moreover, in June, the IEA updated its outlook for 2019 and released projections for 2020 that again suggest oil markets will be oversupplied.

There is an important anomaly that is pointing to sustained tightness in the physical market: the term structure.

An oil market is said to be in contango when the future price for oil is higher than the current spot price. When the future price is below the spot price, the market is said to be backwardated. While it may seem counterintuitive, when the oil market is well supplied, the future price trades above the spot price (contango). In a physically tight market, the future price actually trades below the spot price (backwardation).

To understand why, consider that the future price of oil equals the current spot price plus the cost of capital and the storage cost less the “scarcity premium.” This last term is the premium an oil trader is willing to pay to have crude delivered immediately. In a normal, well-supplied market, the scarcity premium is de minimis relative to the cost of capital and storage cost and the future price trades above the spot price resulting in contango. However, when the physical market is very tight, the scarcity premium will overwhelm the cost of capital and storage and the spot price will actually trade higher than the far-dated futures contracts.

Despite the fact that most analysts continue to think the oil market is oversupplied, both WTI and Brent were backwardated from October 2017 to November 2018 and once again from early 2019 to present. Today, the 12-month WTI backwardation is running at $2.11 per barrel while the Brent backwardation is $2.61 per barrel.

While the conventional wisdom suggests the oil markets are in a sustained glut, the pronounced backwardization tells us that there is no truth in this belief. There is enough physical tightness in today’s market to bid up the near-term oil price for immediate delivery in excess of the future-dated contracts. This is a very unusual divergence and one that suggests the consensus bearish view is ultimately wrong.

This blog contains excerpts of our in-depth commentary, "The Gold Bull Market is Here". If you are interested in this subject, we encourage you to download the full commentary here.