Prefer to listen to this article? Please click the play button above.

The article below is an excerpt from our Q4 2023 commentary.

Over the last sixteen months, weak grain prices have left traders extremely bearish, especially in markets unaffected by the ongoing El Nino. Due to El Nino, India, southern Asia, and West Africa have suffered near drought conditions since June 2023. As a result, the main crops in these regions, notably cocoa and palm oil and, to a lesser extent, wheat, have seen prices fall by much less.

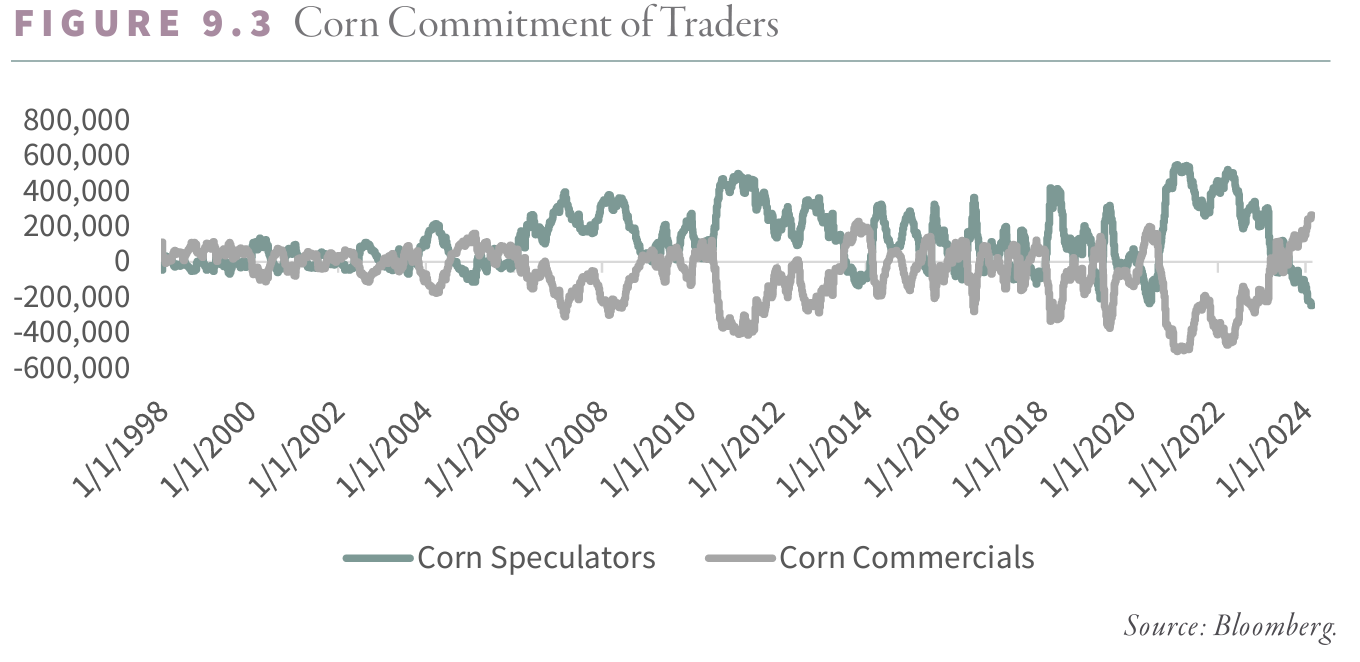

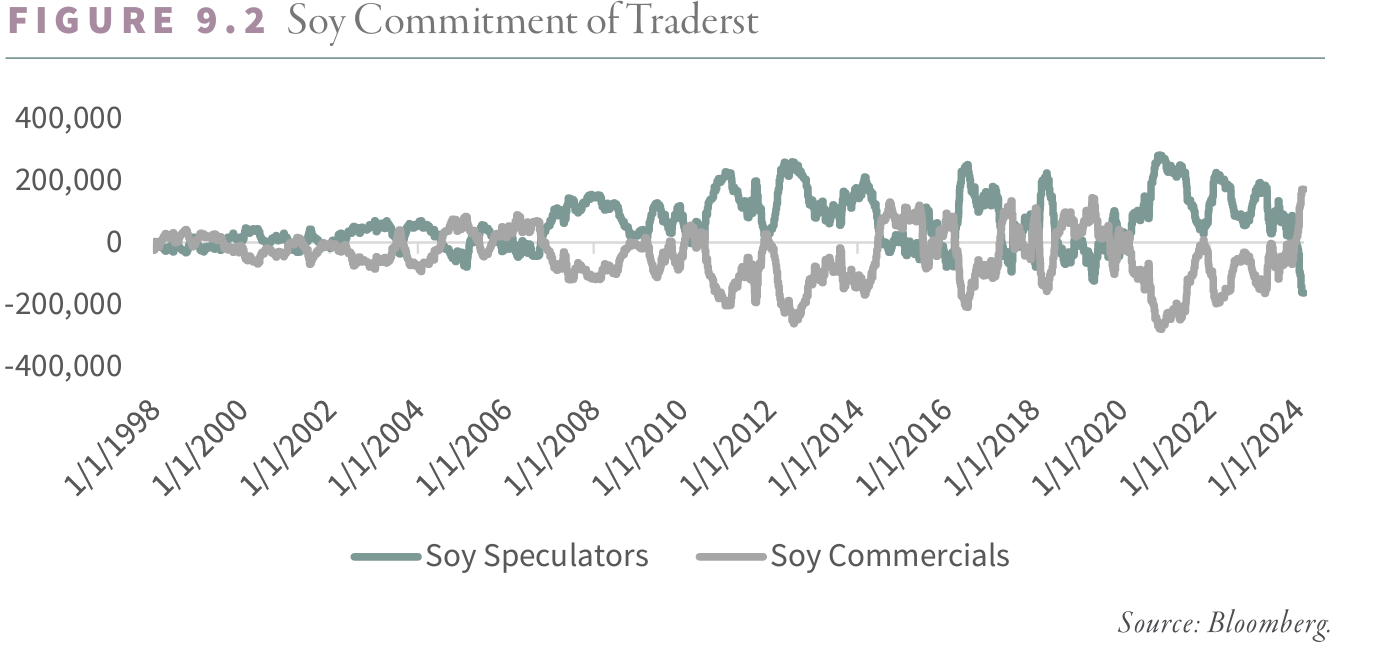

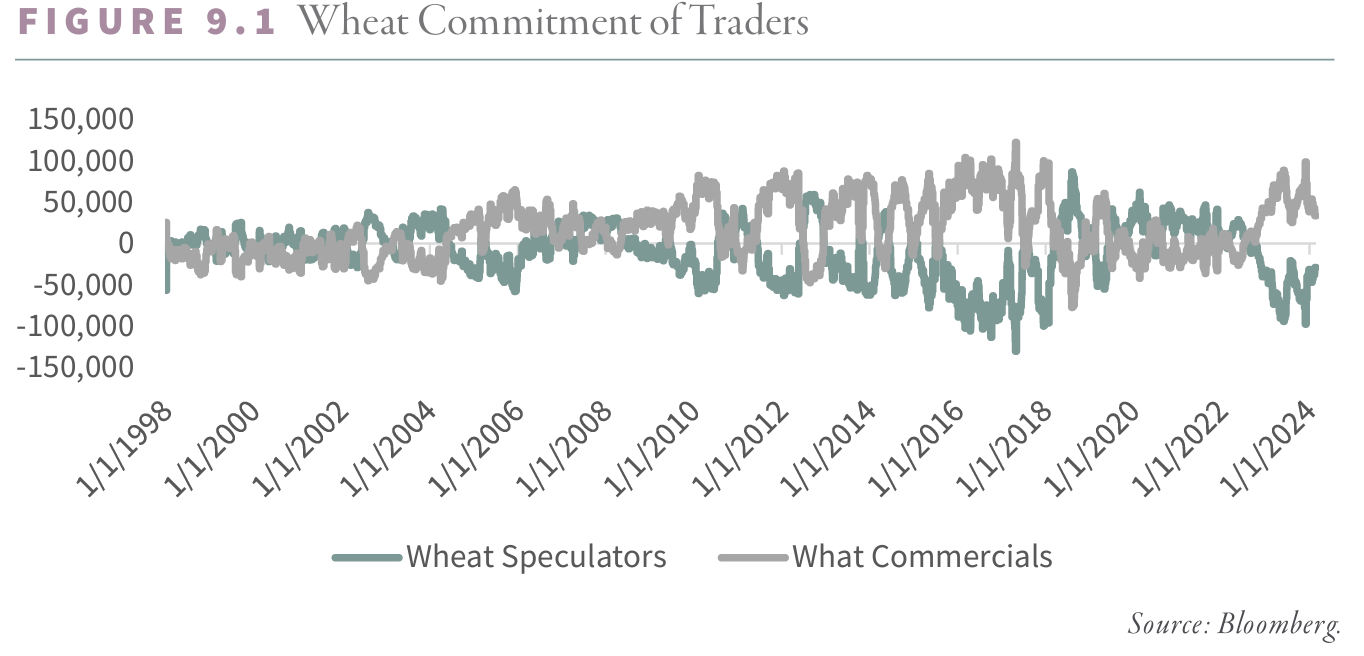

We study the positioning of both speculators and commercial traders on the various futures exchanges. Often, when commercial grain traders hold net long positions, grain prices rise. Commercial traders represent the “smart” money and, under normal market conditions, maintain a net short position to hedge their long physical inventory. A cereal maker must hold large corn inventories and will turn to the futures market to hedge this exposure, resulting in a net short commercial position. On rare occasions, commercial traders will close out their hedges and maintain net long positions. Although rare, a net long commercial position suggests that the “smart” money is worried about future crop supply and is a bullish indicator. Since a net short position must offset every net long position, speculators (i.e., trend followers) are usually net long when the commercials are net short. When the commercial traders turn net long, the speculators will often turn net short, taking the other side of the trade.

Having commercials net long and speculators net short has in the past indicated a significant buying opportunity. Speculators in corn and soybeans now have near-record net short positions, rivaling the extremes last seen in 2019 and 2020 for soy and corn, respectively. Wheat speculators are also short, albeit not at quite the same extreme levels as corn and soy. Corn and soy commercial traders are at near-record net long positions. Wheat commercial traders are also significantly net long, but not at the same extreme levels as corn and soy. The last time corn speculators were this net short and commercials were this net long was June 2020, at which point corn bottomed at $3.15 per bushel. Corn was 160% higher two years later, reaching $8.15 per bushel. The last time soy speculators were this net short was May 2019, at which point prices bottomed at $8.00 per bushel. Over the next two years, soy more than doubled. In wheat, speculators were this net short last in January 2018, at which point prices bottomed at $4.00 per bushel before surging nearly four times over the next four years.

We believe the current positioning indicates that grain prices are poised to enter a potentially massive bull market. The eighteen-month sell-off is likely nearing an end. Investors should position themselves accordingly.

Intrigued? We invite you to download or revisit our entire Q4 2023 research letter, available below.

Registration with the SEC should not be construed as an endorsement or an indicator of investment skill, acumen or experience. Investments in securities are not insured, protected or guaranteed and may result in loss of income and/or principal. Historical performance is not indicative of any specific investment or future results. Investment process, strategies, philosophies, portfolio composition and allocations, security selection criteria and other parameters are current as of the date indicated and are subject to change without prior notice. This communication is distributed for informational purposes, and it is not to be construed as an offer, solicitation, recommendation, or endorsement of any particular security, products, or services. Nothing in this communication is intended to be or should be construed as individualized investment advice. All content is of a general nature and solely for educational, informational and illustrative purposes. This communication may include opinions and forward-looking statements. All statements other than statements of historical fact are opinions and/or forward-looking statements (including words such as “believe,” “estimate,” “anticipate,” “may,” “will,” “should,” and “expect”). Although we believe that the beliefs and expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such beliefs and expectations will prove to be correct. Various factors could cause actual results or performance to differ materially from those discussed in such forward-looking statements. All expressions of opinion are subject to change. You are cautioned not to place undue reliance on these forward-looking statements. Any dated information is published as of its date only. Dated and forward-looking statements speak only as of the date on which they are made. We undertake no obligation to update publicly or revise any dated or forward-looking statements. Any references to outside data, opinions or content are listed for informational purposes only and have not been independently verified for accuracy by the Adviser. Third-party views, opinions or forecasts do not necessarily reflect those of the Adviser or its employees. Unless stated otherwise, any mention of specific securities or investments is for illustrative purposes only. Adviser’s clients may or may not hold the securities discussed in their portfolios. Adviser makes no representations that any of the securities discussed have been or will be profitable. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio.