The article below is an excerpt from our Q1 2023 commentary.

Conventional oil production has now unequivocally rolled over. Unconventional production, the only source of growth in global oil supply over the last 12 years, has also significantly slowed. The only growing non-OPEC basin is the Permian in West Texas. Never before has oil supply growth been so geographically concentrated. Six counties in West Texas are now 100% responsible for all global production growth.

Conventional non-OPEC oil production peaked in 2007 at 46.2 mm b/d and now stands at 44.2 mm b/d – 4% below its peak. Including OPEC, conventional global output peaked in 2016 at 84.5 mm b/d and now stands at 81.3 m b/d – 5% below its peak. Even if OPEC has its alleged 4 mm b/d of unused production capacity (something we do not believe), conventional production would barely regain its 2016 peak.

In 2009, we tried to predict non-OPEC production growth based on every major project expected to come online over the next ten years. Based on our modeling, non-OPEC supply would begin to contract by about 200-400,000 b/d annually. New fields would not grow enough to offset underlying field depletion that we estimated at 4% in the non-OPEC world. In our 2Q18 letter, we tackled the subject again. In two essays (“Conventional Oil: The Problems No One is Talking About” and “Conventional non-OPEC Oil in Depth: Declines are Set to Rapidly Accelerate”), we discussed how conventional non-OPEC production was in terminal decline. Our research looks to have been correct.

However, the world has enjoyed a great luxury—it could ignore the problems firmly embedded in conventional oil production. Surging production from non-conventional oil sources more than offset these declines.

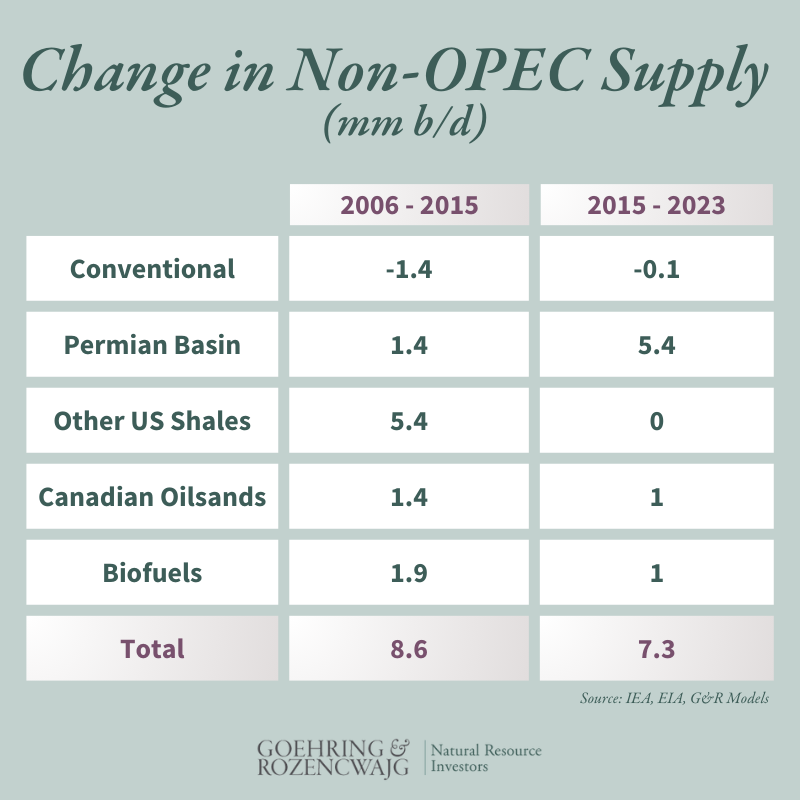

Non-OPEC oil production between 2006 and 2015 grew by 8.6 mm b/d. Conventional oil supply contracted by 1.4 mm b/d. Unconventional oil supply more than offset these declines, surging by 10 mm b/d and broken down as follows: US shales grew by 6.8 mm b/d (65% of all growth), bio-fuels grew by 1.9 mm b/d (19% of the growth), and Canadian oil sands increased 1.4 mm b/d (14% of the growth). Please note that out of this 10 mm b/d growth figure, the Permian represents only 1.4 mm b/d or 14%.

Between 2016 and 2023, unconventional production surged by another 7.4 mm b/d, representing all non-OPEC supply growth. US shales accounted for 85% of the increase. However, whereas all the major shale basins grew from 2006 to 2015, only the Permian grew afterward. The Bakken and Eagle Ford peaked at 1.5 mm b/d in 2015, and this year are each expected only to be between 900,000 and 1 mm b/d. Significant unconventional growth also came from natural gas liquids production in the liquids-rich Marcellus and Utica, which we estimate each added 1 m b/d. This source of production growth is now set to fade, while the plateauing of the Marcellus will turn into a decline.

Between 2006 and 2015, the Permian represented only 14% of unconventional supply growth. Between 2015 and 2023, the Permian represented almost 75% of this growth.

Conventional production started declining in the non-OPEC world over a decade ago. Conventional oil production has most likely turned negative in the OPEC world as well. Over the last thirty years, global oil supply growth has come from multiple geographic areas, including the North Sea, Mexico, Brazil, West Africa, and the Former Soviet Union. Over the last decade, however, these areas have had slight growth, and specific basins, such as the North Sea, have experienced considerable declines.

Consensus opinion believed global oil demand would peak in 2019 and gradually decline through this decade. Just the opposite has occurred: demand has come roaring back post-COVID. Global demand in 1Q23 surpassed 102 mm barrels per day -- three million barrels above the 1Q19 (pre-COVID) level and almost 2 mm b/d above the International Energy Agency’s (IEA) 1Q23 estimate. Strong demand and faltering supply led OECD countries to release 250 mm barrels of oil from their strategic petroleum reserves to keep prices from surging. Given the seasonality in demand and China’s ongoing reopening, the 4Q23 demand could surpass 104 mm b/d.

From here on out, just six counties in West Texas must meet all global demand growth. Given the strategic importance of the Permian, it’s imperative to understand its underlying health. Using our neural network, we have updated our basin analysis, and the results are shocking. The Permian is likely less than a year from peaking and starting its decline. The only source of non-OPEC supply growth is now primarily tapped out.

After many false starts, Hubbert’s Peak is finally here.

Intrigued? We invite you to download or revisit our entire Q1 2023 research letter, available below.

Registration with the SEC should not be construed as an endorsement or an indicator of investment skill, acumen or experience. Investments in securities are not insured, protected or guaranteed and may result in loss of income and/or principal. Historical performance is not indicative of any specific investment or future results. Investment process, strategies, philosophies, portfolio composition and allocations, security selection criteria and other parameters are current as of the date indicated and are subject to change without prior notice. This communication is distributed for informational purposes, and it is not to be construed as an offer, solicitation, recommendation, or endorsement of any particular security, products, or services. Nothing in this communication is intended to be or should be construed as individualized investment advice. All content is of a general nature and solely for educational, informational and illustrative purposes. This communication may include opinions and forward-looking statements. All statements other than statements of historical fact are opinions and/or forward-looking statements (including words such as “believe,” “estimate,” “anticipate,” “may,” “will,” “should,” and “expect”). Although we believe that the beliefs and expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such beliefs and expectations will prove to be correct. Various factors could cause actual results or performance to differ materially from those discussed in such forward-looking statements. All expressions of opinion are subject to change. You are cautioned not to place undue reliance on these forward-looking statements. Any dated information is published as of its date only. Dated and forward-looking statements speak only as of the date on which they are made. We undertake no obligation to update publicly or revise any dated or forward-looking statements. Any references to outside data, opinions or content are listed for informational purposes only and have not been independently verified for accuracy by the Adviser. Third-party views, opinions or forecasts do not necessarily reflect those of the Adviser or its employees. Unless stated otherwise, any mention of specific securities or investments is for illustrative purposes only. Adviser’s clients may or may not hold the securities discussed in their portfolios. Adviser makes no representations that any of the securities discussed have been or will be profitable. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio.