The article below is an excerpt from our Q3 2024 commentary.

In the tumult of the global gold market, the past four years have unfolded as a clash of opposing forces. On one side, the steady drumbeat of rising real interest rates beginning in early 2021 prompted Western investors to liquidate gold holdings with an enthusiasm as familiar as it is predictable. Conversely, an equally determined cadre of global central banks emerged as voracious buyers, amassing reserves with a resolve that seemed to shrug off conventional market pressures.

Initially, it appeared the sellers were winning. By the third quarter of 2022, the price of gold had fallen 20% from its highs. Yet, as often happens in markets governed by crosscurrents, the story took an unexpected turn. Central bank buying surged to unprecedented levels in 2022, ultimately overwhelming Western selling. The result was a sharp reversal: gold prices began a remarkable ascent, climbing steadily through 2023 as central banks continued their buying spree. By the middle of 2024, the gold price had vaulted over 70% above its 2022 lows, an extraordinary feat given the headwinds.

However, the market appears poised on the brink of a fundamental transformation. Central banks, though still buyers, have eased back from the feverish pace of the past two years. Meanwhile, the tide of Western investor sentiment, long bearish, seems to be turning. Declining real interest rates are enticing these erstwhile sellers to reverse course. Between October 2020 and May 2024, the eighteen physical gold ETFs we track collectively shed 1,200 tonnes, rivaling the massive outflows of 2012–2015. But since mid-May, these same ETFs have pivoted, accumulating 150 tonnes—a decisive shift that mirrors broader changes in sentiment.

Silver, often the forgotten sibling of gold, tells a parallel story. From 2021 through early 2024, Western investors liquidated physical silver holdings with abandon, reducing ETF reserves by 13,000 tonnes—two-thirds of the silver amassed during the buying phase of 2019–2021. Yet here, too, the tide has turned. Since May, these ETFs have added 2,500 tonnes of silver, echoing the shift in gold markets.

The current buying phase starkly contrasts the brief resurgence of Western gold demand following Russia’s invasion of Ukraine. Then, gold ETFs accumulated nearly 400 tonnes within two months, but the rally proved short-lived, lacking confirmation from the silver market. Today, the synchronized accumulation of gold and silver suggests a deeper, more sustained shift.

Central banks remain in the picture, albeit with a somewhat reduced role. In the third quarter of 2024, they purchased 186 tonnes of gold, down 40% from the same period a year earlier. The Polish National Bank led the charge, adding 42 tonnes to bring gold to 16% of its reserve assets, with plans to push that figure to 20%. India followed, adding 13 tonnes in the third quarter after purchasing 18 tonnes in each of the first two quarters. Noticeably absent was China, which, after dominating as the largest central bank buyer in 2023, has now sat out for two consecutive quarters—a pause that reflects the dampening effect of gold’s recent price surge.

For 2024, total central bank purchases through the first three quarters reached 694 tonnes—a 17% decline from 2023’s record-breaking pace, yet still the third-highest on record. These figures suggest that central banks, while no longer driving the bus, remain key players in what could be a historic transition in global monetary regimes.

Similar seismic shifts occurred in the early 1930s, the late 1960s, and the turn of the millennium. While the specifics of the impending change remain elusive, the outcome—a serious debasement of fiat currencies relative to gold and other real assets—seems all but inevitable. The price of financial assets will be debased relative to gold and other real assets which happened in the four other monetary regime changes that took place last century. The subject of monetary regime change and its impact on gold prices is a subject we have extensively covered in previous letters.

If central banks set the stage for gold’s recent rally, the return of Western investors could amplify the narrative. Gold prices are in the midst of a substantial bull market, yet investors interest in gold equities remain eerily muted. By several metrics, gold stocks today are as cheap as they were in 1999–2000, a period marked by deep skepticism and relentless selling from European central banks. For more details on the cheapness of gold stocks, please consult our 2Q24 letter.

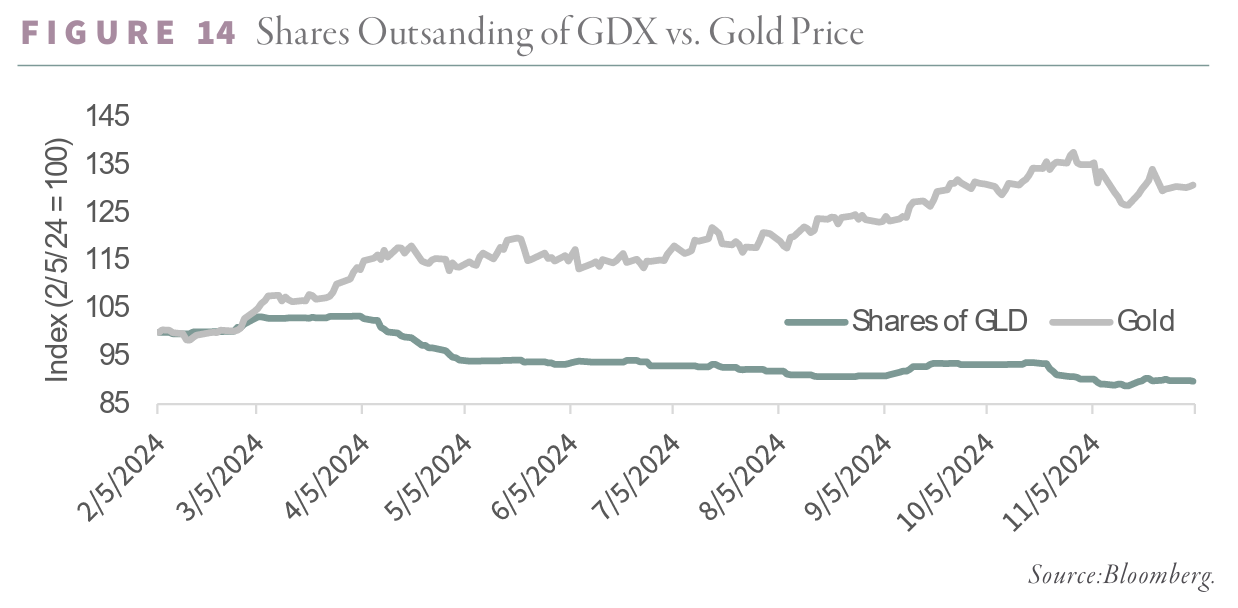

Despite a 15% rise in gold prices since our last letter, the GDX—the most widely held gold equity ETF—has seen outstanding shares shrink by 5% over the past three months. Since gold’s breakout in March, GDX shares have contracted by nearly 20%, even as gold prices climbed over 30%. This peculiar divergence—the rising price of gold versus waning interest in gold equities—is a study in investor psychology.

The chart below illustrates this anomaly, juxtaposing the advancing gold price against the declining shares outstanding of GDX.

For all the fascination with the “Magnificent Seven” tech stocks, the numbers tell a different story. While the QQQ ETF, which tracks the NASDAQ 100, is up 23% year-to-date, gold and gold equities, as measured by the GDX, have risen 38% and 34%, respectively. Yet the broader investing public remains fixated on tech, oblivious to the quiet outperformance of precious metals.

We believe we are witnessing the early stages of a gold bull market that will run for years. The current disinterest in gold equities represents a remarkable opportunity for contrarian investors. Gold stocks will likely be viewed as indispensable assets when this bull market reaches its zenith. For now, however, the prevailing disinterest offers a golden—if undervalued—opportunity.

Curious to learn more? Read more in our Q3 2024 research newsletter, available for download below.

Registration with the SEC should not be construed as an endorsement or an indicator of investment skill, acumen or experience. Investments in securities are not insured, protected or guaranteed and may result in loss of income and/or principal. Historical performance is not indicative of any specific investment or future results. Investment process, strategies, philosophies, portfolio composition and allocations, security selection criteria and other parameters are current as of the date indicated and are subject to change without prior notice. This communication is distributed for informational purposes, and it is not to be construed as an offer, solicitation, recommendation, or endorsement of any particular security, products, or services. Nothing in this communication is intended to be or should be construed as individualized investment advice. All content is of a general nature and solely for educational, informational and illustrative purposes. This communication may include opinions and forward-looking statements. All statements other than statements of historical fact are opinions and/or forward-looking statements (including words such as “believe,” “estimate,” “anticipate,” “may,” “will,” “should,” and “expect”). Although we believe that the beliefs and expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such beliefs and expectations will prove to be correct. Various factors could cause actual results or performance to differ materially from those discussed in such forward-looking statements. All expressions of opinion are subject to change. You are cautioned not to place undue reliance on these forward-looking statements. Any dated information is published as of its date only. Dated and forward-looking statements speak only as of the date on which they are made. We undertake no obligation to update publicly or revise any dated or forward-looking statements. Any references to outside data, opinions or content are listed for informational purposes only and have not been independently verified for accuracy by the Adviser. Third-party views, opinions or forecasts do not necessarily reflect those of the Adviser or its employees. Unless stated otherwise, any mention of specific securities or investments is for illustrative purposes only. Adviser’s clients may or may not hold the securities discussed in their portfolios. Adviser makes no representations that any of the securities discussed have been or will be profitable. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio.