The article below is an excerpt from our Q1 2022 commentary.

Between 2010 and 2020 the world grew accustomed to cheap, abundant conventional energy. Global energy markets were so well supplied for so long that neither investors nor consumers gave energy markets much thought. We were one of the few warning that an impending energy shortage and crisis would emerge in the next several years. The calm of the past decade has been turned upside down seemingly overnight. Conventional wisdom holds that today’s energy shortage is the result of Russia’s invasion of Ukraine; however, we strongly believe this is incorrect. While Russia’s invasion has made the energy shortage much worse in the short term, the underlying problems have been building for many years and cannot be easily remedied.

Our biggest short-term problem is that we are now running out of spare oil pumping capacity. In every prior energy shortage, including the dual oil crises of the 1970s and the rally of 2008, OPEC maintained ample spare capacity that could quickly be brought online. In past letters, we explained why the second half of 2022 would mark the first time in history that global demand bumped up against total pumping capacity.

As we begin to run out of spare capacity, we are only starting to see what that world looks like and, unfortunately, investors still do not appreciate the huge impact this will have. Energy related equities have now significantly outperformed the general stock market over the last two years and yet, investor interest remains extremely low. As far as we can tell, few investors have repositioned their portfolios at all.

Internally, we have discussed what we should expect to see as the world runs out of spare pumping capacity. Although extremely challenging and uncertain, we find it valuable to lay out a roadmap with mile makers that we should expect to pass if our premise is correct. We agreed that if we are in fact running out of spare capacity, we should see a series of large releases from strategic petroleum reserves. On March 31st 2022, President Biden announced he would release a record 1 m b/d for six months from the SPR. Other countries followed suit and agreed to release another 1 m b/d for at least two months.

Historically, SPR releases have been unsuccessful in reducing oil prices and instead are an indication that the physical crude market is exceptionally tight. The larger the release, the tighter the market. The recent announcement from the US and the rest of the International Energy Agency (IEA) member countries is by far the largest coordinated SPR release in history and we believe confirms our thesis that the oil market has fundamentally changed. On the surface, the releases were blamed on the war in Ukraine; however, we believe the true reason is something much more fundamental: if we are running out of spare capacity at some point, oil must be released from the SPRs.

There is no doubt the conflict in Ukraine is making energy matters worse; however, it’s not the complete story. The war in Ukraine is only eight weeks old while the crude market has been in sustained (albeit not widely appreciated) deficit for nearly two years. If we want to ultimately fix today’s energy crisis, we must acknowledge its underlying causes. The record deficit we are now experiencing is the result of a decade of chronic underinvestment combined with relentlessly strong demand. Unfortunately, reversing these factors will take years—an easy and quick fix to the energy crisis is nearly impossible.

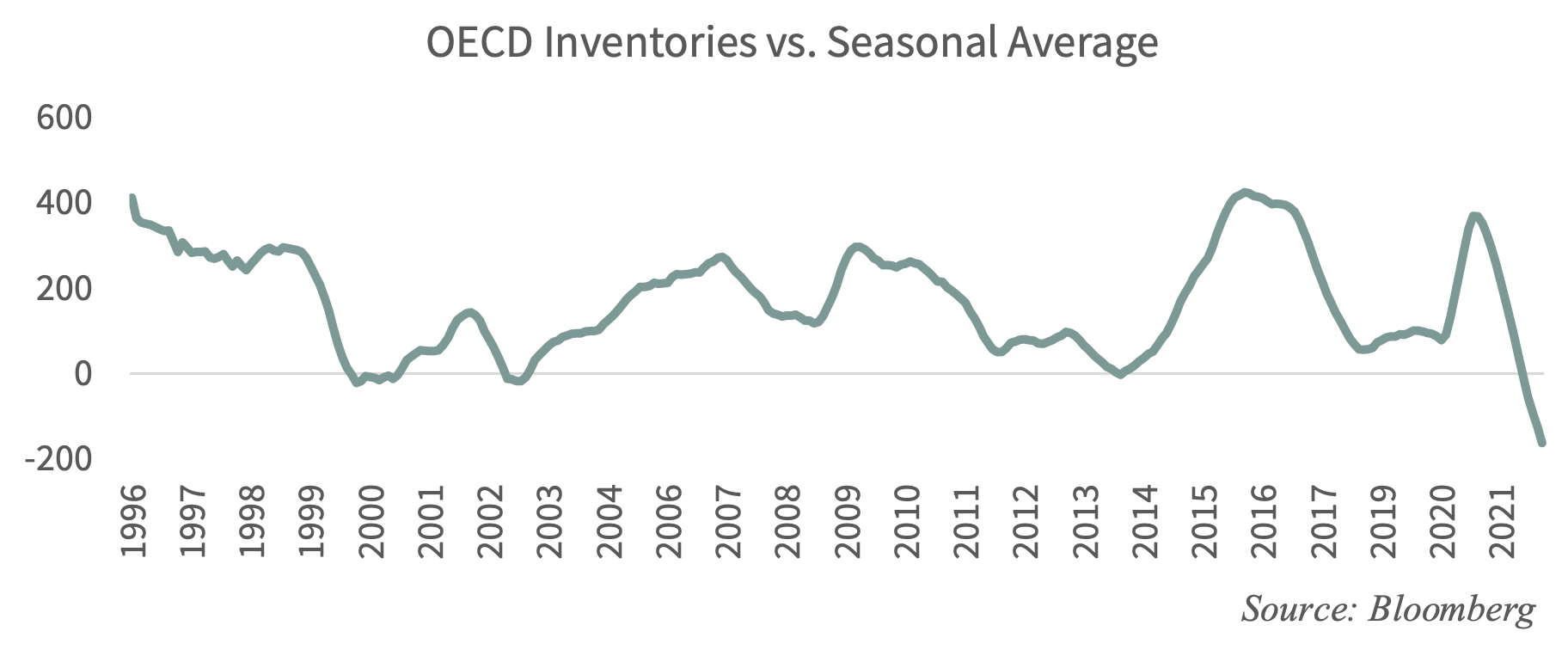

OECD inventories (a good proxy for global inventories) peaked at the height of COVID-19 related restrictions in July 2020 at 4.8 bn bbl – 380 mm bbl above the 10-year seasonal average. Just as global inventories peaked -- along with bearish investor sentiment -- we wrote that we were on the verge of an energy crisis. Demand was likely to rebound much faster than supply, pushing oil markets into severe deficit and resulting in strong inventory drawdowns. Since then, inventories collapsed by 1.2 m b/d, the fastest sustained rate in history. In their latest release, the IEA estimates that OECD inventories ended February at less than 4.1 bn bbl, the lowest absolute level since 2007 and the lowest level relative to 10-year seasonal averages since our dataset begins in 1980. This all took place before Russia invaded Ukraine on February 24th.

More recent data from the Energy Information Agency (EIA) shows US inventories drew counter seasonally again in March and April and that in recent weeks these draws accelerated from 1 m b/d to 1.8 m b/d. Given that the US makes up nearly 50% of total OECD inventories, we expect upcoming data releases will confirm global deficits are quickly getting much worse.

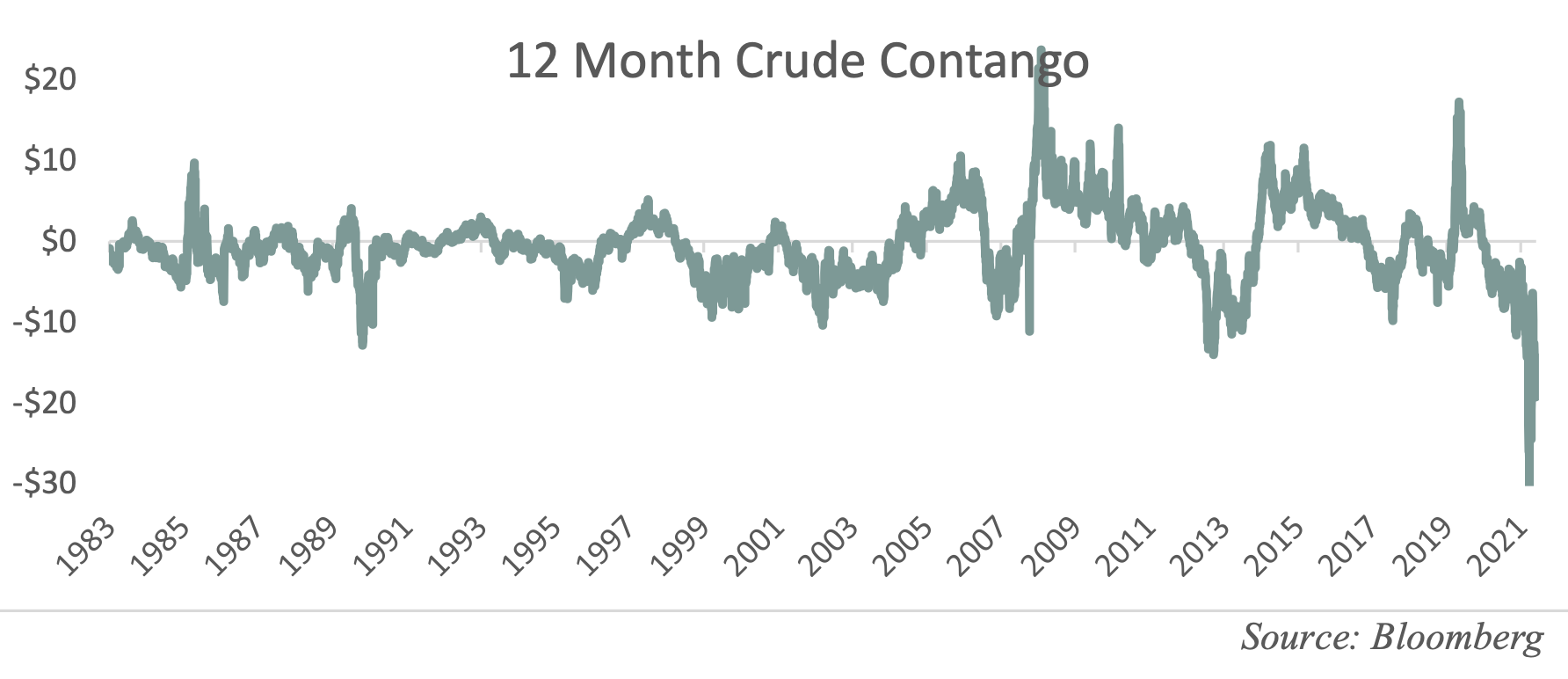

The term structure of WTI and Brent are both signaling extreme physical market tightness. Under normal circumstances a commodity contract for delivery in the future will trade at a premium to the prompt month contract, reflecting the costs of capital and storage. In periods of acute shortage, physical traders are willing to pay a premium for prompt delivery, pulling the near-term contract above the later-month contract – a situation known as backwardation. Currently, physical markets are so tight that traders are willing to pay a record $17 premium (or nearly 15%) for oil delivered promptly compared to a year from now. We have never seen this level of anxiety or market tightness.

Years of underinvestment in upstream oil and gas projects has produced the present deficit. Trying to reverse this shortfall will take years of upstream capital spending at rates double and triple of what we are spending today. Until we reverse this shortfall in upstream capital spending, we will not fix the underlying problem.

The oil industry is inherently cyclical: high prices lead to strong profitability which attracts investment and ultimately leads to surplus production. Prices then fall, hurting profitability and pushing capital out of the industry. Ultimately shortages arise once depletion takes hold. At the end of the last energy bull market in 2010, inventors worried that “peak supply” would lead to persistent shortages. Crude averaged almost $100 per barrel between 2010 and 2014 and capital poured into an E&P industry that was busy developing the nascent US shale oil fields. Between 2010 and 2019 production grew from nothing to over 9 mm b/d. If the shales were a country, they would have gone from no production to being the world’s third largest producer in just 10 years, behind only Saudi Arabia and Russia. The shales produced more oil than all of Europe, Central and South America combined. It is not an exaggeration to say the shales were the most important oil development since the Saudi super major fields, led by Ghawar, in the early 1950s.

Oil began to collapse at the end of 2014 and capital began flowing out of the sector. Oil and gas capital spending fell by over 60% between 2010 and 2020. Investment in the US shales fell by over 70%. Over that entire period, the cumulative reduction in capital spending compared to trend was more than $1 tr.

Over the same period, ESG concerns came to grip the global investor community. We believe much of the capital needed to build renewable projects was diverted away from upstream oil and gas investment. Unfortunately, wind and solar are intermittent sources of power that suffer from very poor energy efficiency. Lithium-ion batteries, necessary for both buffering intermittent renewables and powering electric vehicles, are also extremely energy intensive to mine and manufacture. Our research tells us that neither wind, solar nor electric vehicles, because of their poor energy efficiency, will live up to their promise of replacing oil and gas. Please see our Q4 2021 letter where we discuss the limitations of wind and solar. We now know the incredible growth of shale oil (and shale gas), and the resultant downward pressure it put on oil and gas prices, fooled investors into thinking they could divert huge amounts of capital into unproductive renewable projects without any consequences. What are those consequences and how painful are they going to be? We are only now beginning to find out.

In a normal cycle, falling inventory levels, rising prices, and improved profitability would have attracted capital back into the industry by now. Instead, ESG commitments made over the past several years are keeping capital from reentering the oil and gas industry, making the production problems much worse. Oil prices are at 15-year highs and natural gas in Europe and Asia are setting new records and yet E&P capital spending is still down 50% from the peak with shale spending down 60%. Despite record free cash flow, companies prefer to return capital through dividends and share buybacks rather than drill new wells. Several E&P executives were brought before Congress last fall and criticized for not doing more to curtail their fossil fuel production. These same companies were called to Washington again in April and asked why they were not producing more. Unfortunately, the impact of many years of anti-fossil fuel rhetoric cannot be undone overnight.

Another major issue facing the energy industry is that, although the shale resource is extremely large, it is ultimately finite just like any other conventional field. Like a conventional resource, a shale basin ramps up early in its life then plateaus and ultimately declines. We were among the first to intensely study the concept of shale depletion as early as 2019 and we concluded their best days were likely past. This was an incredibly important conclusion given the US shale basins represented nearly 90% of all non-OPEC+ growth between 2010 and 2019. In our Q4 2019 letter, we laid out our research and predicted that shale growth would begin to falter, causing the global crude market to slip into deficit. So far this is exactly what has happened.

We built an artificial neural network to understand the factors driving shale productivity growth. Immediately, we realized the industry was preferentially drilling its best wells – a process known as high-grading. Instead of improving their drilling techniques (a common industry story at the time) and turning Tier 2 areas into Tier 1 wells, the E&P industry was drilling out the cores of the shale basins at ever-faster rates. We argued that as companies drilled out their Tier 1 inventory, well productivity would soon begin falling, making it far more difficult for the shale basins to grow.

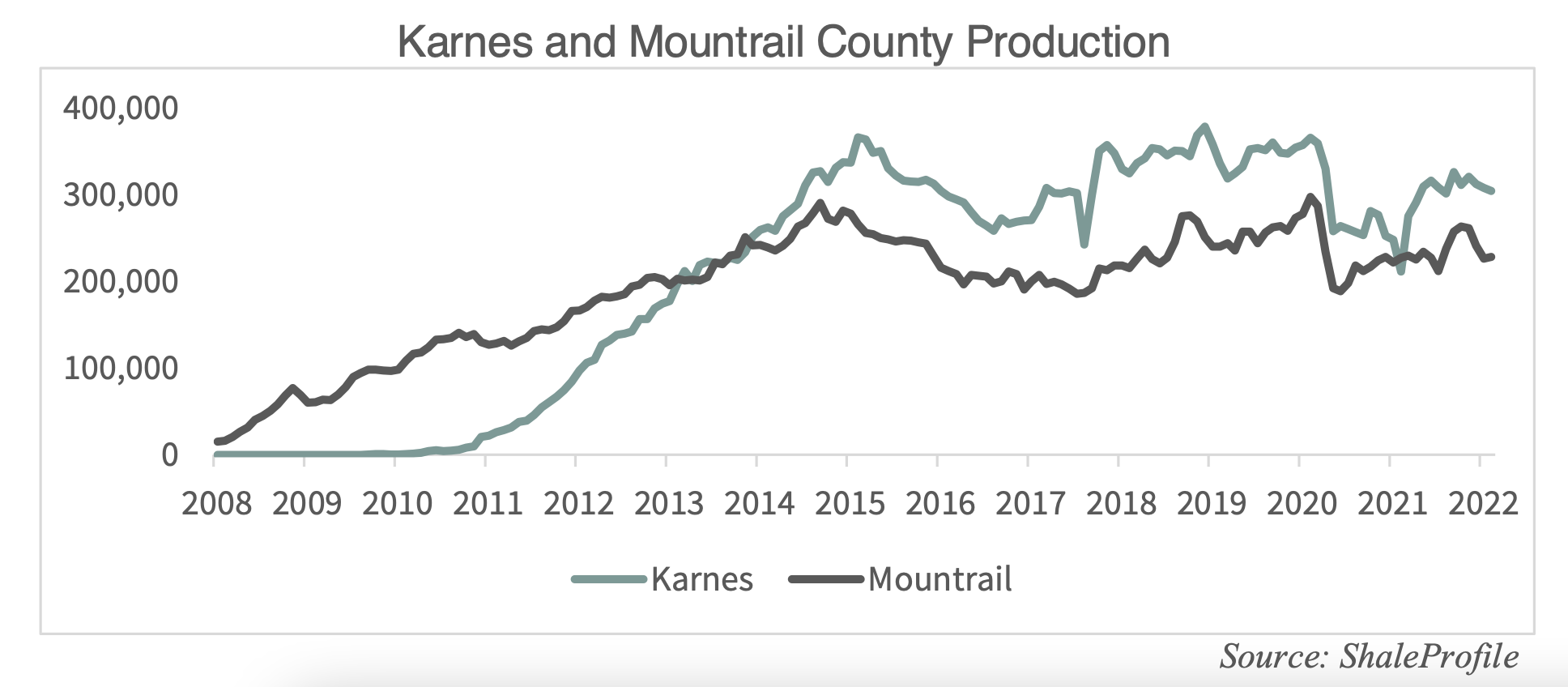

To understand the importance of drilling productivity, we put forth these real-life examples. Consider the best county in each of the Big 3 shale basins: Karnes County in the Eagle Ford, Mountrail County in the Bakken, and Midland County in the Permian. Each of these counties are prime Tier 1 acreage with wells that enjoy production rates nearly twice the average Tier 2 well. Karnes County is 750 square miles. Assuming 6,000 foot laterals and 800 foot lateral spacing, there are at most 3,800 drilling locations representing 23 mm lateral feet of wellbore. To date, we estimate 18 mm of the 23 mm lateral feet have been drilled – or nearly 85%. Out of 3,800 top tier Karnes drilling locations, only 400 remain undrilled today.

Mountrail County, home to the best wells in the Bakken, is larger at 1,900 square miles. Assuming 9,000 foot laterals and 1,300 feet between wells, there is room for at most 3,200 wells in the county totaling 27 mm lateral feet of well bore. So far 19 mm lateral feet have been drilled or 70% of the total. Of 3,200 locations only 700 remain today.

Production from both counties peaked all the way back in 2015, and despite big increases in oil prices between 2016 and 2018, and again today, neither Karnes nor Mountrail counties have been able to grow production.

Both counties saw production ramp, plateau, ultimately make a second peak, and then roll over. Today both counties remain 50,000 b/d below their pre-Covid level. As these basins run out of undrilled locations, operators have been forced to look to lower quality parts of the basin, hurting productivity. In the Bakken, per well productivity peaked in December 2019 and has since fallen by 6%. In the Eagle Ford, productivity has held in better but only because total completions remain down by over 40% compared with 2019. Eagle Ford companies have been able to keep their well productivity high by reducing completion activity by nearly half and focusing only on their remaining high-grade inventory. Clearly this trend cannot last. If companies lack high-quality Tier 1 drilling locations, production will continue to disappoint.

Despite being both the youngest field and having the most drilling locations, even the Permian is not immune from the early stages of resource depletion. Midland County is 900 square miles of the best acreage in the entire Permian basin. Assuming 10,000 foot laterals, 1,300 feet between wells, and three productive zones of stacked Wolfcamp pay (very generous), we believe there are at most 3,900 drilling locations in Midland county representing 39 mm lateral feet of wellbore. Thus far, 24 mm feet have been drilled implying Midland County is over 60% developed. Although Midland production is still growing, our models believe this will likely soon begin to plateau as well.

Permian Tier 1 exhaustion might be happening already. Between late 2019 and March 2022, Permian per well productivity has fallen by a very large 14% even though completions remain down 7%. The only source of non-OPEC+ growth over the past decade is now suffering resource exhaustion, just like any other conventional resource. We predicted this trend in late 2019 and if our models continue to be correct, then production will soon begin to disappoint materially.

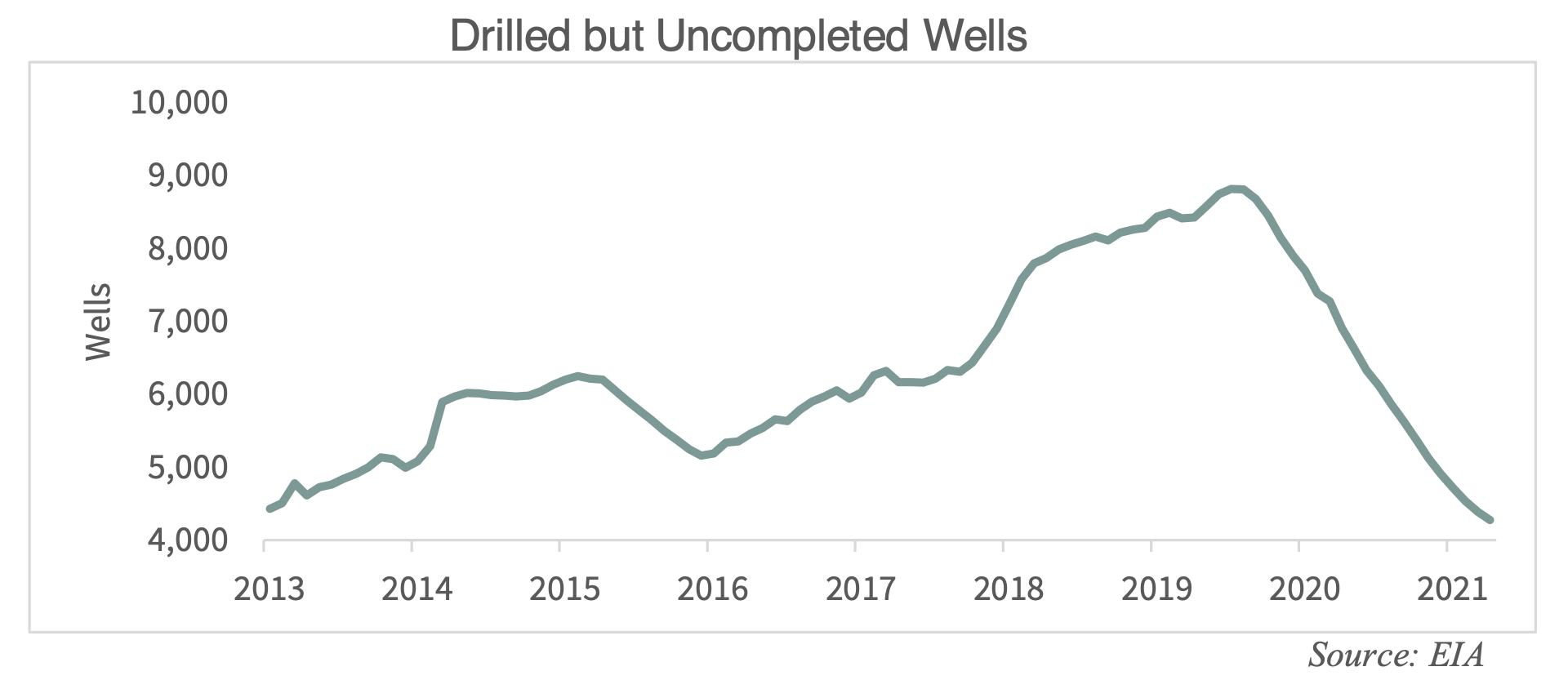

In aggregate, productivity in the Big 3 shale basins is down 6% compared with 2019 and production remains 550,000 b/d below the peak. In other smaller shale basins, the declines have been more dramatic with production now 450,000 b/d below the peak (on a smaller base). Moreover, we estimate that nearly 1 mm b/d of incremental production came from the completion of drilled but uncompleted wells (DUCs). These wells were drilled in the lead-up to COVID-19 but ultimately not completed when oil prices collapsed. In 2021, energy companies completed 50% more wells than they drilled as they drew down their DUC inventory, leading to a one-time boost in production. Today, there are fewer than 4,300 DUCs – the lowest level since our dataset began in 2013. Clearly the industry needs some DUC inventory to properly function, and we believe we have now reached that level. The past four months saw sequential shale growth in excess of 100,000 b/d but, if our models are correct regarding DUC liquidation, this will slow dramatically as we progress into the summer.

Conventional US production continues to fall precipitously, having declined by 16% since its peak while Gulf of Mexico production is off 20%. Higher oil prices have not helped either source of supply: conventional US production is off 7% year-to-date while the Gulf of Mexico is down 6%.

Non-OPEC+ production outside of the US was supposed to have been a bright spot in 2022 (something we never agreed with) but is now severely disappointing as well. In the first four months of the year, the IEA has revised 4Q21 and 1Q22 estimates lower by a material 300,000 b/d. In a pattern that has repeated itself many times, the IEA revised down the actual data while revising higher the second half estimates, leaving the full-year figures unchanged. The IEA now expects non-OPEC+ production outside of the US to reverse course and grow by a staggering 1.2 m b/d over the next two quarters – something we believe to be impossible. To put this in proper context, production from this group is now down 500,000 b/d over the past six months versus original estimates calling for growth of 500,000 b/d.

At the same time as production is disappointing, demand is running far ahead of expectations. In our past letters, we explained how the IEA has embedded a chronic demand underestimation into its forecasts, largely driven by flaws in its emerging market methodology.

In 10 of the last 12 years, the IEA has ultimately been forced to revise its demand estimates higher by 1 m b/d on average and this problem is getting worse. In their February 2022 report, the IEA undertook the largest series of demand revisions in their history. Going back to 2018, the IEA revised global demand higher by nearly 1 mm b/d each year on average with nearly all the revisions focused on the emerging markets. This was followed up with a smaller set of upward demand revisions in March of nearly 200,000 b/d on average going back to 2019.

Even after these historic revisions, we believe the IEA is still underestimating demand. In the first quarter of 2022, the IEA claims that global supply averaged 98.7 m b/d while demand averaged 98.5 m b/d, suggesting inventories should have built by 200,000 b/d. Instead, preliminary data points to inventory draws between 500,000 and 600,000 b/d. In other words, the “missing barrels” are back: that is oil that was produced but neither consumed nor added to inventory. Our readers know that the “missing barrels” are usually under-reported non-OECD demand and we believe this time will be no different. In the first quarter, we estimate that even after the historic revisions, the IEA continues to underestimate demand by as much as 800,000 b/d. If this demand continues – and we have every reason to believe it will – the crude market is even tighter than most people currently realize.

One question we are often asked is whether high prices will curtail demand and potentially push the world into recession. The topic of demand destruction is extremely interesting and in a future letter we will likely dedicate a whole essay to the subject. Using the relationship of oil expenditures to GDP helps us put the current situation in proper context. The last two major oil tops occurred in 1980 when oil rallied from $3 to $36 per barrel and in 2008 when oil rallied from $11 to $145 per barrel. In 1980, the US consumed 17 m b/d which amounted to $225 bn per year on GDP of $2.9 trillion. In other words, nearly 8% of US GDP was spent on oil. On a global basis, oil demand averaged 61 m b/d, amounting to $800 bn on GDP of $11 trillion, or 7.2%. In 2007, the US consumed 19 m b/d, amounting to $1 tr on GDP of $14.5 tr, or 6.9%. Globally, we consumed 86 m b/d, amounting to $4.5 tr or 7.8% of $58 tr in global GDP.

At present, the US consumes 20 m b/d, amounting to $730 bn at $100 per barrel crude. With GDP running at $21 tr, oil expenditures amount to 3.5% -- less than half the prior two peaks. Globally, demand ran at 97.5 m b/d last year (although we believe this is higher), amounting to $3.4 tr or only 4% of global GDP – again only slightly more than half the prior two peaks. Oil prices likely contributed to slowing economic growth in 1980 and 2008, however we are not yet at the same levels of expenditures. Were oil to reach $170 per barrel, expenditures as a percentage of GDP would reach 6-7%, more consistent with previous market tops. We actually believe, for a variety of reasons, that a figure closer to $150 per barrel would put undue pressure on the economy, and in our upcoming letter we will discuss our rationale.

With demand running higher than expectations and non-OPEC+ supply disappointing, all eyes are on OPEC+. President Biden asked the cartel to produce more oil in November 2021 and again in February 2022 and both requests were ignored. Most analysts we speak with believe that OPEC+ (led by Saudi Arabia) chose not to increase production; however we believe they tried but were ultimately unable to. In our past letters we have detailed extensively why we believe OPEC+ spare capacity is much lower than anyone realizes. As of March 2022, nearly every OPEC+ country was producing below their allotted quota – something we never recall seeing. The core OPEC-10 countries produced nearly 1 m b/d less than allowed, effectively leaving $3 bn in revenue on the table in March alone while the remaining member countries missed their quota by 700,000 b/d. There is no logical explanation for why this should happen consistently, as it has, other than the member countries have been unable to increase production. The argument that OPEC+ is somehow aiding Russia by keeping prices high also seems unlikely. Saudi Arabia serves as the de facto leader of OPEC+ and is very skeptical of Russia. As recently as March 2020, Russia and Saudi Arabia were engaged in an outright price war within OPEC+ that was partially responsible for taking prices negative. Furthermore, Russia’s support of Iran in various proxy fights is fundamentally opposed to Saudi Araba’s interests. Instead of cooperating to the detriment of NATO and the West, we believe OPEC+ in general (and Saudi Arabia in particular) found they were unable to boost production in March – another sign we are now running out of global spare pumping capacity.

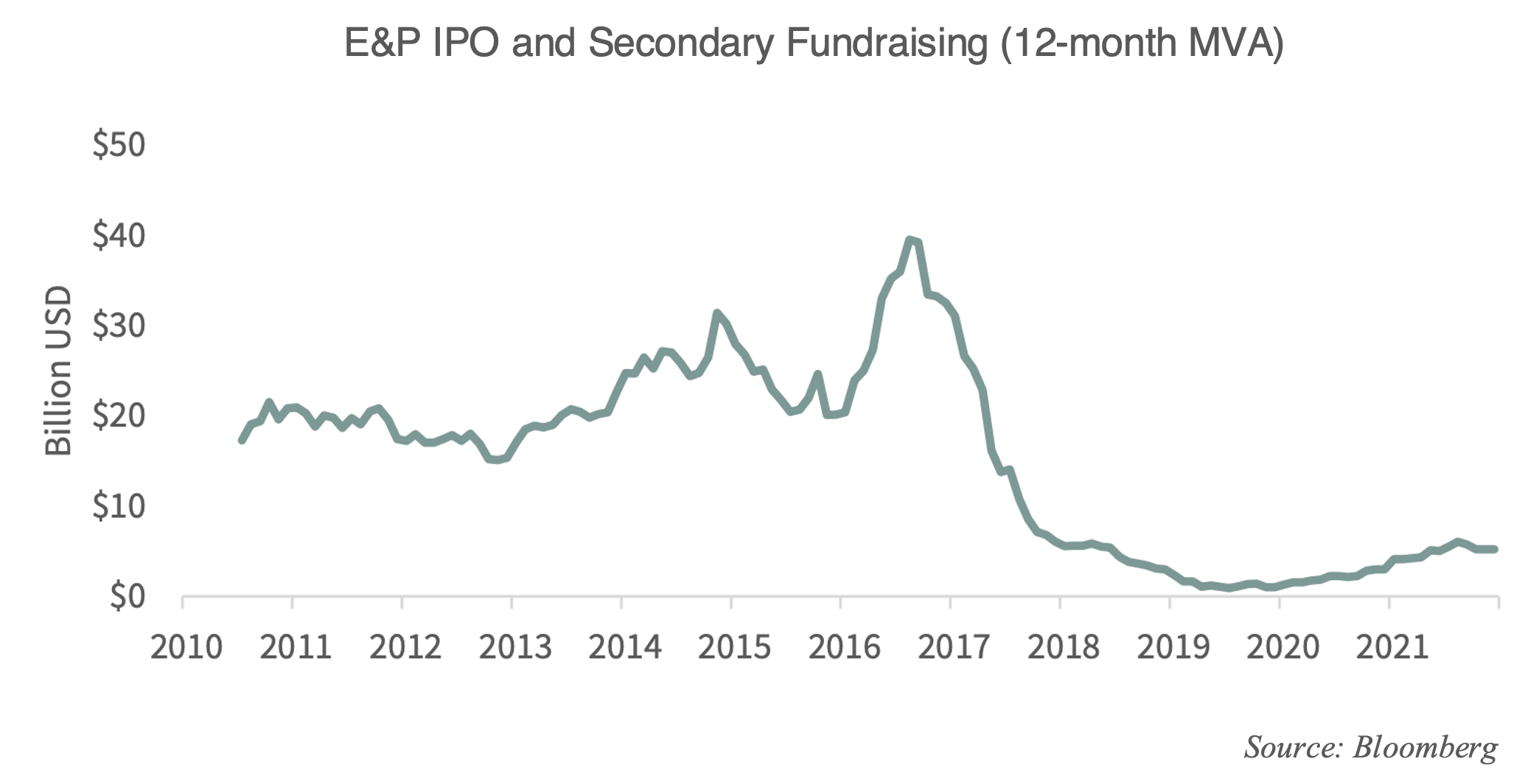

The current energy crisis will not be solved until capital comes back into the industry in significant quantities. Normally high commodity prices and improved profitability help attract capital, but ESG pressures are keeping that from happening. E&P capital budgets are indeed up 25% compared with the 2021 lows, however they remain 60% below trend-line. Moreover, we are hearing that most of the increase is not the result of increased activity but rather represents cost inflation as bottlenecks have now developed in key equipment, steel, and labor. Energy related IPOs and secondary offerings totaled a mere $1.8 bn over the past six months, 80% below the $10 bn average between 2010 and 2017 and 90% below the $22 bn peak in 2016.

Capital remains unavailable even though oil and gas prices are high and even energy hostile politicians are now calling for more upstream investment. Investor interest in the energy sectors also continues to be extremely low. Between January 2021 and today, the XOP (the largest ETF of E&P stocks) has advanced by 120% and yet, over that period, the shares outstanding have actually decreased--investors have actually redeemed shares on balance.

We are now beginning to understand what a world looks like as it runs out of spare oil pumping capacity. Even with the huge releases of oil from Strategic Petroleum Reserve, oil prices have hardly pulled back. Global inventories, now at record lows, continue to draw counter-seasonally and are reaching dangerously low levels. Even with all the dislocations caused by the Ukrainian conflict and COVID problems in China, global oil demand in Q4 will approach global pumping capability according to our modelling. Strong demand, declining production, record low inventories, and now no spare pumping capacity—all these factors will push oil prices higher in the second half of 2022. Even in the face of all these factors, investor interest in energy markets remains incredibly subdued. The advances we have seen to date have basically been short covering and active managers buying on the margin. Once investors and institutions realize the energy market has fundamentally changed and the decade of cheap, abundant energy is over, the amount of capital that rushes into this sector could be huge. The global energy crisis has just started, and it will take many years to fix. For those that make investments today, the rewards could be immense.

Intrigued? We invite you to revisit our entire Q1 2022 research letter, The Gas Crisis is Coming to America, available below.