The article below is an excerpt from our Q3 2024 commentary.

The great drama of American shale production may now be nearing its final act. For years, we have anticipated that the relentless growth in shale output would crest by late 2024 or early 2025, catching many off-guard. In hindsight, even this expectation might have erred on the side of caution. Quietly and without much fanfare, both shale oil and shale gas appear to have passed their zenith several months ago. Recent data from the Energy Information Agency (EIA) reveal that shale crude oil production reached its high-water mark in November 2023, only to slide 2%— roughly 200,000 barrels per day—since then. Likewise, shale dry gas production peaked that same month and has since slipped by 1% or 1 billion cubic feet per day. The trajectory from here, according to our models, looks steeper still.

Our view has been met with no shortage of skepticism. Many of our conversations with clients and industry insiders suggest a broad belief that today’s declines are but a pause, not a prelude to sustained contraction. Optimists contend that higher prices and a deregulatory push will spark a new wave of drilling and fresh production gains. After all, President-elect Trump’s “Three Arrows” energy plan prominently promises a 3-million-barrel-per-day increase in US oil-equivalent production. But we see this optimism as misplaced. The primary forces behind the current downturn are neither policy-related nor purely economic—they are geological and inexorable. Depletion, not market dynamics or regulatory overreach, is the central culprit.

Admittedly, the incoming administration features several well-informed and capable figures in the energy sphere, including Chris Wright and Scott Bessent. Their leadership will undoubtedly foster a favorable climate for drilling activity. Yet, even with their expertise and the administration’s likely zeal for energy development, we remain convinced that these efforts will struggle to offset the entrenched declines now gripping the shale sector. The geology of the shale patch has spoken, and its verdict seems increasingly final.

Our thesis is built upon the enduring insights of the late Dr. M. King Hubbert, whose groundbreaking prediction of the peak in conventional U.S. crude production in 1970 remains a landmark in energy analysis. In this essay, we aim to show how we have adapted Hubbert’s foundational work, augmenting it with the latest advances in artificial intelligence, neural networks, and machine learning to address the complexities of shale production. The implications of our findings are profound. Our edge lies in an uncommon synthesis: the marriage of cutting-edge computational techniques with deep, domain-specific expertise in the energy sector.

Too often, we observe legacy oil and gas analysts tethered to antiquated models, while AI practitioners—adept at the math but unfamiliar with the nuances of resource extraction—arrive at flawed conclusions. Neither approach alone suffices anymore. Our unique combination of skills allows us to reach conclusions that defy conventional wisdom, and we are confident these conclusions will ultimately prove prescient.

Let us explain why.

In recent months, we’ve engaged with a range of investors and oil industry executives. While many grasp the logic behind our analysis, few are ready to accept its implications. At a recent talk before an audience of oil and gas operators at the Houston Petroleum Club, the most common counterargument boiled down to this: if shale production continues to decline, higher prices will follow. And with higher prices, operators know precisely where to drill next. Each operator, brimming with confidence in their ability to boost production, assumes that the industry as a whole will do the same.

The rationale seemed straightforward: with the rig count far below previous peaks, availability is unlikely to be a bottleneck. While the remaining drilling locations might be less productive, they could still yield acceptable returns at elevated oil and gas prices. Given the vast number of undrilled but economically marginal locations, operators were convinced that U.S. shale production would rebound swiftly, negating any nascent rally in prices.

Yet, as we will argue, this collective confidence may rest on shaky ground. The factors driving shale’s decline are far more structural than the industry at large appears willing to admit.

Our models point to a sobering conclusion: even with substantially higher prices and an abundance of undrilled locations, production is set to continue its decline. We call this phenomenon the “depletion paradox.” It is a familiar story, and history provides a clear precedent.

Consider the case of conventional U.S. crude production in the 1970s. Production peaked in November 1970 at 10 million barrels per day, with oil priced at just $3.18 per barrel. At that time, the industry operated a modest 302 rigs drilling for oil. The first OPEC oil crisis in 1973 sparked a response from President Nixon in the form of Project Independence—a sweeping initiative aimed at reversing the decline in U.S. output through deregulation and expedited permitting. Much like today, optimism abounded among oil producers, who believed that higher prices would unleash a drilling boom and restore U.S. production growth. They were confident they knew where to drill; all they needed was the right price signal.

Prices soared from $3.18 per barrel in 1973 to $34 per barrel by 1981. Producers, true to their promises, responded with vigor. The rig count climbed from 993 in 1973 to a staggering 4,500 by late 1981. Yet despite this unprecedented surge in drilling activity, U.S. oil production steadily declined throughout the 1970s. By the end of 1981, production had fallen to 8.5 million barrels per day—far below the peak achieved a decade earlier and lower than when Nixon announced his ambitious goals.

Three decades later, in 2010, U.S. oil production hit a nadir of 5 million barrels per day, even as prices hovered around $100 per barrel—30 times higher than in 1973. The depletion paradox had firmly taken hold. The industry’s assumption—that higher prices alone could counteract geological realities—proved tragically flawed. Today, as we observe the shale sector grappling with similar dynamics, it seems history may once again be repeating itself.

We believe the U.S. shale sector now stands at a crossroads eerily similar to that faced by conventional oil production in 1973. While shale’s achievements have been extraordinary, they remain subject to the inexorable forces of depletion. Yet, the industry, Wall Street, and the President-elect appear poised to repeat the missteps of half a century ago.

The lessons of history are clear: enthusiasm for growth, however well-intentioned, cannot override the fundamental constraints of geology. And if we fail to heed these lessons, we risk not just disappointment, but the stark realization that higher prices and bold policy initiatives are no match for depletion’s steady advance.

King Hubbert – a History

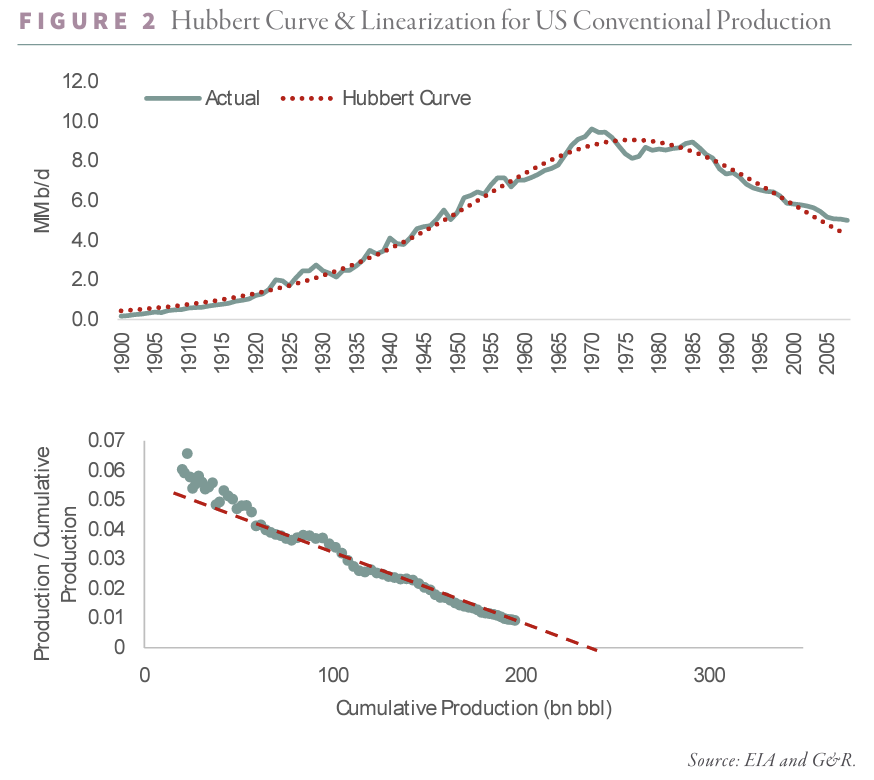

M. King Hubbert, a geologist for Shell, was born in 1903 and left an indelible mark on the study of petroleum resources. In 1956, during a meeting of the American Petroleum Institute, he presented a bold prediction: U.S. oil production would peak in 1970 at around 10 million barrels per day. At the time, his assertion seemed audacious, even implausible—after all, U.S. production had been rising steadily since Colonel Drake’s first successful well nearly a century earlier. Hubbert faced significant skepticism, but history proved him right. In November 1970, just as he had forecasted, U.S. production reached its apex and began its long decline.

Although Hubbert’s name is widely associated with the concept of “peak oil,” surprisingly few have taken the time to engage deeply with his original work. His conclusions may have sparked controversy, but the principles underpinning them are remarkably straightforward.

Hubbert’s central argument was simple yet profound: every hydrocarbon basin is a finite resource. As such, the cumulative production of a field will follow a predictable trajectory. It begins at zero, rises as extraction ramps up, and ultimately reaches an upper limit that represents the total recoverable resource in the basin. When plotted over time, cumulative production inevitably traces a curve with this general shape:

While Hubbert acknowledged that the exact profile of production could vary widely, he emphasized that it would always slope upward—what mathematicians call “monotonically increasing”—as cumulative production can only grow, never shrink. For instance, a field developed rapidly might display a near-vertical rise, while one extracted at a steady pace might show a slower, more linear progression before reaching its upper bound.

Hubbert proposed using a logistic curve to approximate this behavior. The logistic curve forms a smooth, symmetrical “S” shape: it starts at zero, accelerates as production ramps up, and eventually approaches a fixed value, which represents the basin’s total resource. This elegant model captured the essential dynamics of resource depletion and provided a framework that has shaped energy forecasting ever since.

Taking the derivative of cumulative production with respect to time reveals the field’s production profile. For a logistic cumulative production function, this derivative yields a bell-shaped curve, perfectly symmetric around its peak—a hallmark of Hubbert’s framework.

Hubbert also introduced a second groundbreaking concept: his eponymous “linearization.” By plotting the ratio of annual production to cumulative production (P/Q) against cumulative production (Q), he observed that after an initial period of variability, the relationship settled into a straight line. This insight provided a powerful analytical tool. By extrapolating the line to the point where P/Q reaches zero, one could estimate both the field’s ultimately recoverable reserves and the coefficient of its production profile. With these two parameters in hand, constructing a Hubbert Curve became straightforward, allowing analysts to predict both the timing and magnitude of a field’s production peak.

One of Hubbert’s key insights was that a field typically reaches its peak when half of its reserves have been extracted. While intuitively satisfying, this idea raises an intriguing paradox: why should production stop growing when half of the field’s reserves still remain? The answer lies in the complex interplay between depletion and production dynamics—a concept that underscores the limits of extraction and the inevitability of decline, even in the presence of significant remaining resources. This “depletion paradox” remains a cornerstone of modern resource analysis.

The paradox has vexed petroleum engineers since Hubbert first introduced it. Frustratingly, Hubbert himself was unable to offer a satisfying explanation from first principles. He openly acknowledged that his choice of a logistic curve—and the resulting bell-shaped production profile—was not rooted in theory but rather in its consistent empirical success.

The logistic curve, as Hubbert noted, reliably described the production rollovers of many smaller fields he studied during the 1950s. This empirical track record lent the model its credibility and ultimately guided Hubbert to his now-famous prediction of the U.S. oil production peak in 1970. While the curve’s elegance and accuracy cemented its place in resource analysis, the lack of a deeper theoretical underpinning left its critics unconvinced, ensuring the paradox would remain a subject of debate.

Explaining Hubbert – From Macro to Micro

Although the logistic curve has demonstrated its predictive prowess, it’s surprising how little attention has been given to the reasons behind its effectiveness. Much of the criticism aimed at Hubbert’s model arises from this very ambiguity. The curve works—but why? Without a solid understanding of the underlying mechanisms, many find themselves rejecting the “depletion paradox.” After all, wouldn’t higher prices or new technologies accelerate development and override the limits of depletion?

Yet, history has taught us a different lesson. Despite ample profits and a legion of engineers, the industry in the 1970s couldn’t outmaneuver the realities of depletion. To shed light on this paradox, perhaps it’s time to shift our focus from the macro level of entire fields to the micro dynamics of individual wells.

Imagine, if you will, a hypothetical oil field endowed with an infinite number of identical wells, each drilled at a constant rate indefinitely. In such an admittedly unrealistic “infinite” field, one might expect production to grow endlessly. However, the reality is that the field’s output would ramp up and eventually plateau at a fixed rate. This might sound counterintuitive at first glance, but it becomes clear upon closer examination.

In the early days of the field’s development, every new well adds directly to total production. Once these wells are online, they begin to decline in output in a predictable fashion. In the following period, new wells continue to contribute the same volume of fresh production, but now the growth is partially offset by the declining output of the older wells.

As long as the production from new wells exceeds the cumulative declines from existing ones, the field’s overall output continues to grow. However, the base decline—the total reduction from all the aging wells—also increases. The field will keep expanding until the additions from new wells exactly balance out the base declines. At that juncture, the field reaches equilibrium, and total production levels off.

/2024.Q3%20Commentary/2024.12%20Figure%203%20-%20Unlimited%20Identical%20Wells%20Drilled%20Constantly.png)

This scenario illustrates why even infinite potential can’t escape the constraints of depletion. It underscores a fundamental truth: growth is bound not just by resources but by the interplay between new additions and inevitable declines. Higher prices and technological advancements may influence the pace, but they can’t alter the underlying dynamics that eventually lead to a plateau in production.

Of course, no field is truly infinite. Oil and gas deposits are the result of geological processes spanning hundreds of millions of years, and every field’s resource base is, by nature, finite. If we adjust our earlier assumption and consider a field with a fixed number of identical wells drilled at a constant rate until the resource is exhausted, a different production profile emerges. Under these conditions, production initially grows as new wells come online, eventually reaches a plateau, and then falls off sharply. The resulting curve bears little resemblance to the symmetric bell-shaped profile of Hubbert’s logistic model. Instead, the peak occurs much later in the field’s lifecycle, at a point where approximately 80% of the ultimate recoverable reserves have already been extracted.

/2024.Q3%20Commentary/2024.12%20GR%20Figure%204%20Fixed%20Number%20of%20Identical%20Wells%20Drilled%20Constantly%20to%20Exhaustion.png) This revised scenario highlights the impact of finite resources on the dynamics of production. While the plateau phase might offer the illusion of stability, the eventual sharp decline serves as a stark reminder of the field’s limits. It’s a pattern that underscores the inexorable pull of depletion, even when development appears robust and ongoing.

This revised scenario highlights the impact of finite resources on the dynamics of production. While the plateau phase might offer the illusion of stability, the eventual sharp decline serves as a stark reminder of the field’s limits. It’s a pattern that underscores the inexorable pull of depletion, even when development appears robust and ongoing.

More Realistic Examples

Thus far, our examples have been deliberately simplified, designed to illustrate key principles. Of course, no field is infinite, and no prudent oil producer would drill a fixed number of wells without regard to inventory or strategic considerations. These examples, however, provide a useful baseline as we begin to relax assumptions and introduce more realism into the model.

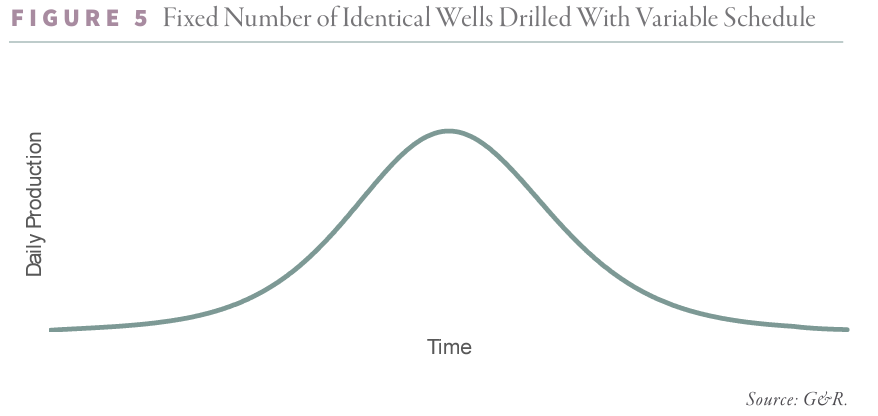

In practice, oil companies face two critical constraints: how much to drill and where to drill. An energy executive must decide how to allocate capital and human resources across a given field. Early in a field’s life, these decisions are marked by uncertainty. The field is unproven, cash flow may be limited, and companies tend to proceed cautiously, drilling slowly at first.

As the field demonstrates its potential and begins to generate cash flow, development accelerates. The goal at this stage is to maximize present value by ramping up activity quickly, deploying more capital and resources to extract as much value as possible. However, this phase doesn’t last indefinitely. As undrilled locations become scarcer, companies naturally slow development. The desire to maintain an adequate reserve life index and the practical constraints on further expansion lead to a deceleration in activity.

Interestingly, the trajectory of the drilling schedule itself often traces a bell-shaped curve. It begins with a slow ramp-up, accelerates to a peak as activity intensifies, and eventually tapers off as the field matures. This pattern mirrors the life cycle of resource extraction and reflects the broader dynamics of balancing opportunity with constraint in the development of finite resources.

If we assume constant well productivity and a logistic drilling schedule, the field’s cumulative production will follow a classic logistic curve, while its production profile will take the shape of a perfect bell curve. In this scenario, production reaches its peak precisely when half of the field’s recoverable reserves have been extracted. This inflection point coincides with the company’s decision to slow drilling activity, marking the transition from growth to decline.

The symmetry of this model underscores the intrinsic relationship between drilling intensity and resource depletion, offering a tidy framework for understanding how production evolves under controlled conditions.

The second constraint oil companies face is where to drill. To maximize net present value, operators typically prioritize their best prospects first. This is true both within a single basin, where they aim to target the “sweet spot,” and across a broader portfolio, where they allocate resources to the most promising basins. As a result, it’s reasonable to assume that, over time, per-well productivity will begin to decline as the best locations are exhausted.

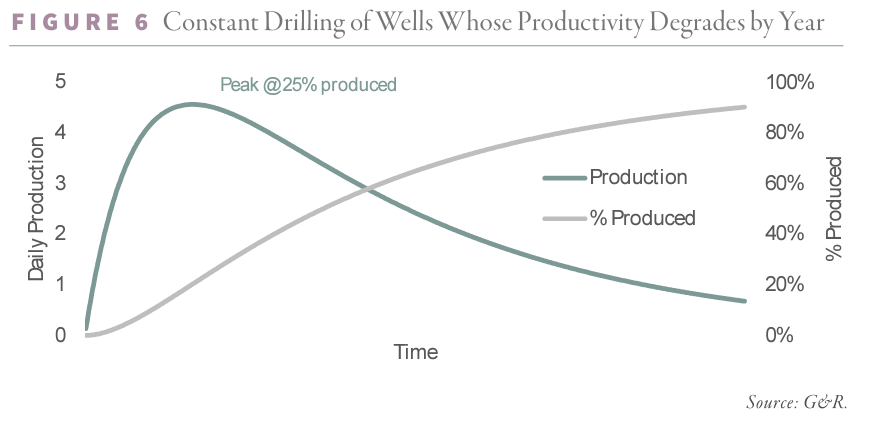

Earlier, we observed that an unlimited number of wells with constant productivity leads to a production plateau. Introducing declining well productivity, however, inevitably results in falling production. If we now assume an infinite number of wells, but drilled in such a way that well productivity steadily degrades, production will exhibit a different trajectory: it will grow, plateau, and then roll over. The decline on the right-hand side of the curve will be more gradual than the initial ramp-up on the left.

For instance, if new well productivity decreases by 5% each year, production peaks after only 20% of the ultimate resource has been extracted. Interestingly, the rate of degradation influences the timing of the peak in a somewhat counterintuitive way. The steeper the degradation, the later the field will reach its peak. A field with new wells declining in productivity by 10% per year, for example, will peak after 25% of its reserves have been produced. This dynamic illustrates how depletion interacts with productivity and timing, shaping the trajectory of production in unexpected ways.

In practice, a constant interplay exists between drilling schedules and well quality. Given the finite nature of resources and the imperative to maximize present value, the pace of drilling becomes a pivotal factor. Drill too quickly, and you exhaust the most productive areas at an accelerated rate. Drill more slowly, and you extend the life of the field, albeit at the cost of delayed returns.

As a result, every field’s production is shaped by a dynamic balance between the rate of drilling and the degradation of well quality over time. The production profile that emerges reflects this delicate equilibrium, with the field’s trajectory dictated by the interplay between resource depletion and development strategy.

Conventional US Production – A Case Study

With a clearer grasp of Hubbert’s principles and the intricacies of well-level development, we might ask: What insights emerge from the downturn in U.S. oil production that began in 1970?

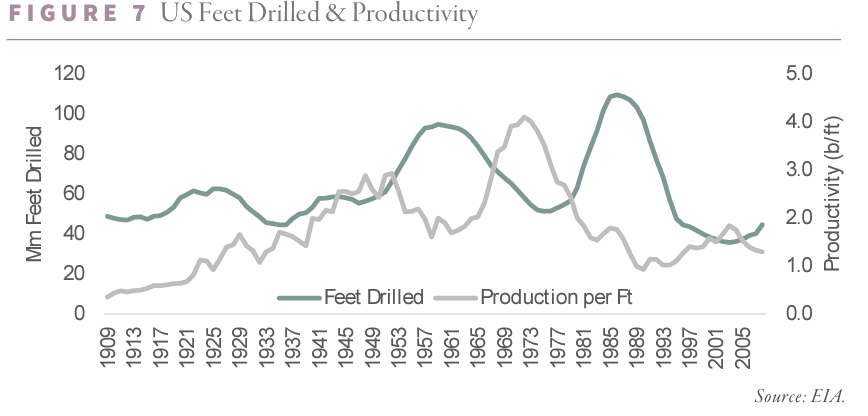

During its growth phase, U.S. drilling activity was remarkably steady. Between 1900 and 1945, the industry consistently drilled about 50 million feet annually. Over this period, as the industry matured, productivity didn’t just increase—it soared. Output per foot drilled grew sixfold, rising from a modest 0.5 barrels per foot to nearly 3 barrels per foot.

By the late 1950s, a significant shift occurred. Drilling activity surged by 70%, reaching nearly 100 million feet. Yet paradoxically, productivity halved to just 1.5 barrels per foot. As a result, new production edged up by only 20%, despite the sharp increase in drilling efforts. As total production expanded, depletion rates climbed as well, trimming net production growth by a third. The U.S. was gradually stepping onto a plateau.

In the late 1960s, production quotas and regulatory measures caused drilling to slow by 40%. This slowdown prompted companies to “high-grade” their inventory, focusing on their most promising prospects. Productivity more than doubled, and gross new production increased by nearly 50%.

Starting in 1970, productivity began its relentless decline as the prime areas of the best fields became fully developed. By the mid-1980s, productivity had fallen by nearly 75%. A surge in drilling activity—spurred by President Nixon’s policies— could not compensate for the plummeting productivity, and gross new production dropped sharply. Total production had peaked in 1970 and continued to fall throughout the decade.

Thus, we see that drilling activity and well productivity often mirror each other inversely. As one rises, the other falls, illustrating the complex dynamics at play in the industry.

The industry, in its way, wasn’t entirely wrong. They did have an abundance of new drilling locations—though of a decidedly lower quality. What they failed to grasp was the unforgiving reality of relentless base declines. It took only a tipping of the scales in new production to trigger a steep and inevitable downturn in overall output.

When examining gross new additions—calculated as productivity multiplied by feet drilled—a striking pattern emerges. This metric forms its own bell-shaped curve, one that closely mirrors the famous Hubbert curve. This played out even with an abundance of available drilling locations and despite high oil prices. The underlying cause? A steady erosion of productivity per foot drilled. The industry was running out of the highest-quality areas to exploit. And once those prime locations were exhausted, increased drilling activity only served to offset gains with corresponding declines in productivity, culminating in the rollover.

The result was a near perfect Hubbert curve, with production peaking once half the recoverable reserves had been produced.

Turning to the Shales

Equipped with our framework, what can we discern about the shale revolution? In many ways, shale basins differ markedly from conventional fields. They are vastly more aerially extensive and boast orders of magnitude more drilling locations. Early shale plays were even likened to “manufacturing processes,” evoking a factory more than a traditional oil field.

Yet shale brings its own complexities. Productivity across a basin can vary dramatically, with the best areas often yielding four times the output of the worst. Applying our earlier reasoning, it’s reasonable to assume that well degradation would take on a larger role, leading to production profiles characterized by earlier peaks and extended right-hand tails. Experience has borne this out.

Another defining feature of shale wells is their distinctive production pattern. They tend to produce at very high rates initially, followed by steep declines, and eventually settle into a prolonged period of low-rate output. This behavior stems from the nature of hydraulic fracturing, which releases a surge of trapped fluid—“flush” production—followed by a slower, drawn-out bleed of fluids from the formation over time.

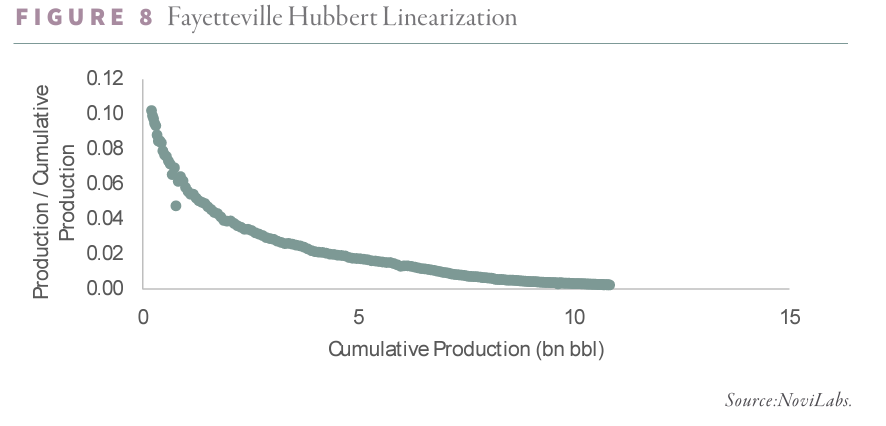

Given these unique dynamics, it’s unsurprising that shale wells defy traditional Hubbert Linearization. When plotting the ratio of production to cumulative production against cumulative production (P/Q vs. Q), the result is no longer a straight line but a curve—a testament to the distinct nature of these wells.

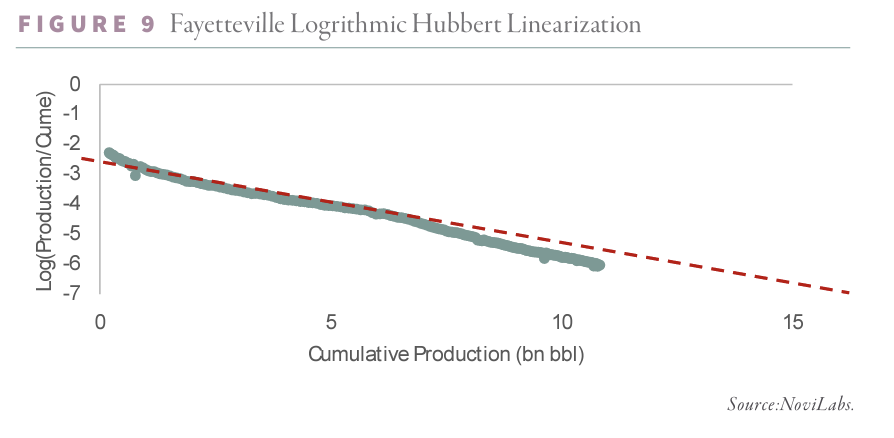

Early analysts often struggled to apply conventional Hubbert Linearizations to shale basins, leading to forecasts that were, at best, imprecise. The difficulty lay in the fact that the production plots were not straight lines. Yet, upon closer examination, a surprising discovery emerged: while the relationship isn’t linear, it is perfectly logarithmic. Plotting the logarithm of P/Q against Q produces a straight line, one that can be extrapolated with remarkable accuracy.

This logarithmic approach enables extremely precise forecasting of shale production profiles. Strikingly, no other analysts or academics appear to have arrived at this conclusion. Using this method, we accurately predicted the rollovers in major plays like the Barnett, Fayetteville, Eagle Ford, and Bakken. These fields have since declined anywhere from 26% to 80%.

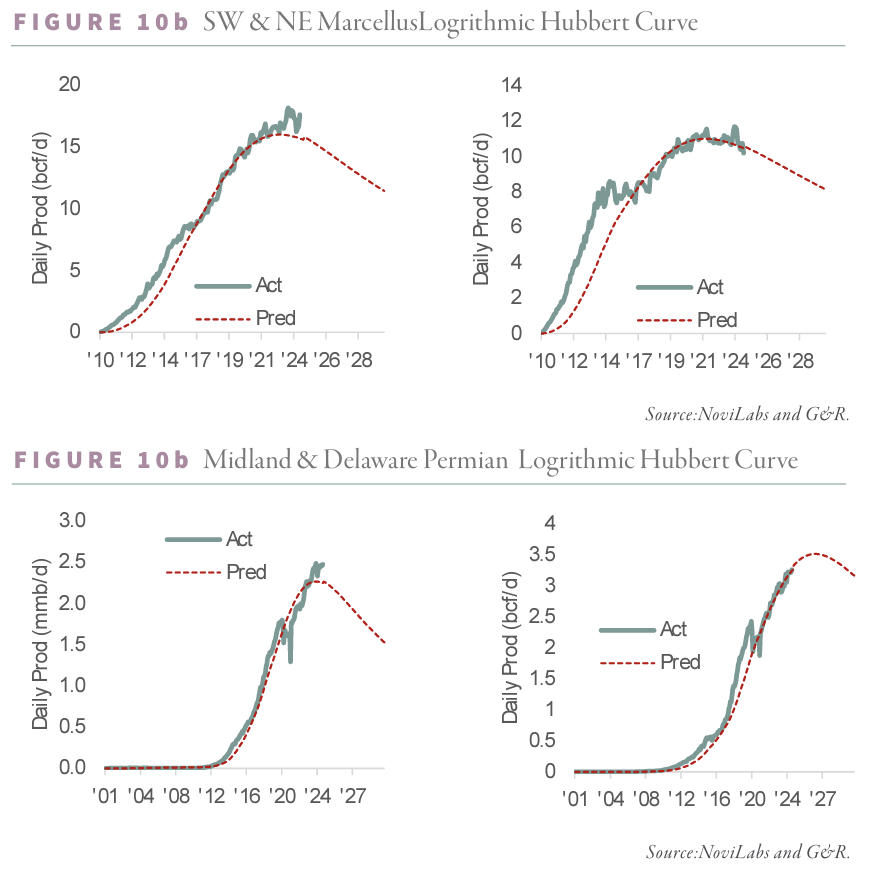

The same analysis now reveals that both subbasins of the Marcellus have rolled over, as has the Midland side of the Permian Basin. The Delaware side of the Permian and the Haynesville are expected to follow shortly.

Beyond predicting rollovers, the logarithmic Hubbert Linearization also captures the longer right tails that are characteristic of shale basins. For instance, the Fayetteville and Barnett production profiles have been distinctly asymmetric, declining more slowly than they ramped up. Our logarithmic model identified this trend with precision.

Beyond predicting rollovers, the logarithmic Hubbert Linearization also captures the longer right tails that are characteristic of shale basins. For instance, the Fayetteville and Barnett production profiles have been distinctly asymmetric, declining more slowly than they ramped up. Our logarithmic model identified this trend with precision.

By applying this tool, we can accurately estimate the recoverable reserves of each basin and predict the timing of peak production. According to the logarithmic Hubbert Curves, most shale basins reach their peak after approximately 30% of their recoverable reserves have been produced. This longer right tail is a hallmark of well degradation and highlights the gradual drilling out of the cores.

Enter Neural Networks

To validate our ultimate recoverable reserve estimates from logarithmic linearizations and explore shifts in well productivity, we turned to artificial intelligence. Frustrated with the limitations of conventional tools, we began developing our own in 2019. The result is a sophisticated toolkit of neural networks and machine learning models, custom-built for the task at hand.

As we’ve noted, our unique position combines deep domain expertise with a strong grasp of artificial intelligence. While AI has become a buzzword, and everyone now claims expertise, we’ve been training and refining deep neural networks since 2019. Unlike the sprawling large language models like ChatGPT, our models are purpose built and pragmatic. Instead of mimicking human thought, they are trained to predict shale well production based on subsurface geology, regional trends, and well completion designs.

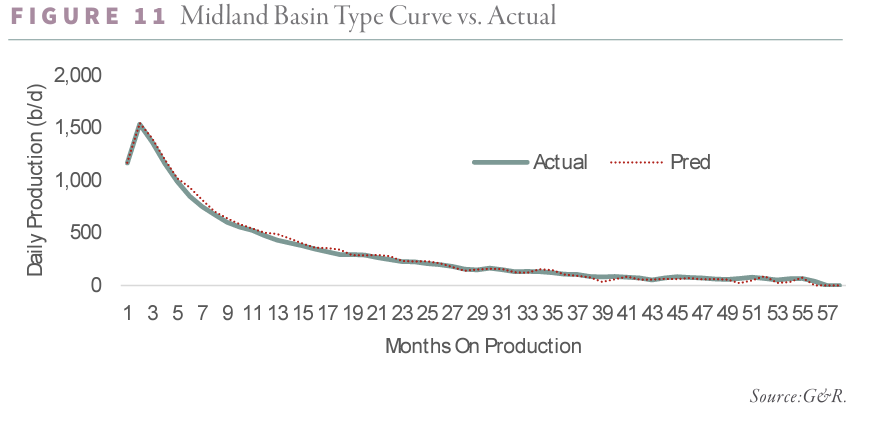

The payoff has been remarkable. For instance, the next chart illustrates our models’ predicted average type curve for the Midland side of the Permian Basin against actual well results, achieving an R² of nearly 0.98.

Since starting this journey, we’ve rebuilt our models several times, each iteration leveraging the latest advancements in technology and architecture. We know encorporate well completion data such as fluid and proppant loading and lateral length; suburface geological data such as permiability, porosity, clay content, thermal maturity, organic content and pressure; geological trend data, itself learned from a deep neural network; and spacing data related to neighboring wellbores. Our current iteration integrates tools like Random Forest models, a deep neural network to uncover hidden geological patterns, and cutting edge methods useful for intrepreting the results. The results are striking.

Since starting this journey, we’ve rebuilt our models several times, each iteration leveraging the latest advancements in technology and architecture. We know encorporate well completion data such as fluid and proppant loading and lateral length; suburface geological data such as permiability, porosity, clay content, thermal maturity, organic content and pressure; geological trend data, itself learned from a deep neural network; and spacing data related to neighboring wellbores. Our current iteration integrates tools like Random Forest models, a deep neural network to uncover hidden geological patterns, and cutting edge methods useful for intrepreting the results. The results are striking.

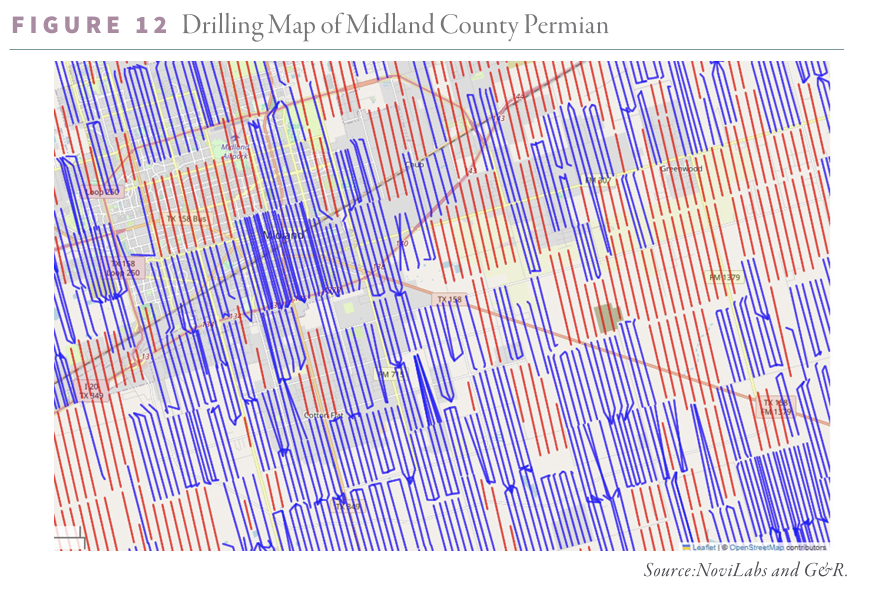

First, we mapped each basin, identifying the remaining drilling locations by formation horizon. For the Midland side of the Permian Basin, it’s clear that many top-tier locations have already been developed. While significant numbers of undrilled wells remain, they are located in far less productive parts of the field.

Next, we estimated the ultimate recoverable reserves for each well—drilled and undrilled—aggregating the results to compare with our linearizations and cumulative production to date. This approach, moving from a “top-down” basin view to a “bottom-up” well-level perspective, confirmed the robustness of our methods. Remarkably, our AI models produced reserve estimates within 15% of the logarithmic linearizations for oil and within 14% for gas.

Across all fields, our linearizations suggest that basins will roll over when approximately 28% of their reserves are produced. Our machine learning models show oil shales are now 28-32% depleted, while gas shales are 30-34% depleted. This points to a slowdown driven by depletion, not price or regulation.

Indeed, total shale oil and gas production likely peaked late last year. Both are already down 1%, and our models predict year-over-year production declines will turn sharply negative within six months.

Depletion Paradox Redux

This slowdown couldn’t come at a worse time. Since 2010, the growth in global oil demand has been entirely met by shale crude and NGLs. Domestically, shale gas production has suppressed prices to 80% below global levels, fueling the largest ever rollout of natural gas-fired electricity generation and LNG export capacity in U.S. history. Yet few have considered the implications of sourcing sufficient feedstock. With Americans consuming as much energy from natural gas as from oil, what happens if prices converge with global levels?

Even with rising prices, we doubt shale production will surge. History offers a lesson. The unexpected production rollover in the 1970s was driven by declining per-well productivity—a pattern we believe will repeat.

Today, 60-70% of all shale production comes from wells less than three years old, making production trends highly sensitive to changes in new well productivity. Yet the remaining undrilled locations are, on average, 35% less productive than wells drilled in 2023, primarily due to inferior geology. This degradation is not easily remedied.

Today, 60-70% of all shale production comes from wells less than three years old, making production trends highly sensitive to changes in new well productivity. Yet the remaining undrilled locations are, on average, 35% less productive than wells drilled in 2023, primarily due to inferior geology. This degradation is not easily remedied.

Should higher prices or deregulation spur drilling activity, the likely outcome would be plummeting productivity, much as occurred in the 1970s. Despite increased drilling, total production would struggle to grow, constrained by the quality of remaining inventory and the relentless pace of depletion.

Between 1973 and 1985, the U.S. drilled more conventional well feet than during any other 13-year period. Yet production still declined. Today, we face a similar paradox: while undrilled locations remain and higher prices may render them economic, it is unlikely they will materially boost total U.S. production. In the end, the paradox remains—depletion is an unstoppable force, and it is becoming harder and harder to keep up.

Curious to learn more? Read more in our Q3 2024 research newsletter, available for download below.

Registration with the SEC should not be construed as an endorsement or an indicator of investment skill, acumen or experience. Investments in securities are not insured, protected or guaranteed and may result in loss of income and/or principal. Historical performance is not indicative of any specific investment or future results. Investment process, strategies, philosophies, portfolio composition and allocations, security selection criteria and other parameters are current as of the date indicated and are subject to change without prior notice. This communication is distributed for informational purposes, and it is not to be construed as an offer, solicitation, recommendation, or endorsement of any particular security, products, or services. Nothing in this communication is intended to be or should be construed as individualized investment advice. All content is of a general nature and solely for educational, informational and illustrative purposes. This communication may include opinions and forward-looking statements. All statements other than statements of historical fact are opinions and/or forward-looking statements (including words such as “believe,” “estimate,” “anticipate,” “may,” “will,” “should,” and “expect”). Although we believe that the beliefs and expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such beliefs and expectations will prove to be correct. Various factors could cause actual results or performance to differ materially from those discussed in such forward-looking statements. All expressions of opinion are subject to change. You are cautioned not to place undue reliance on these forward-looking statements. Any dated information is published as of its date only. Dated and forward-looking statements speak only as of the date on which they are made. We undertake no obligation to update publicly or revise any dated or forward-looking statements. Any references to outside data, opinions or content are listed for informational purposes only and have not been independently verified for accuracy by the Adviser. Third-party views, opinions or forecasts do not necessarily reflect those of the Adviser or its employees. Unless stated otherwise, any mention of specific securities or investments is for illustrative purposes only. Adviser’s clients may or may not hold the securities discussed in their portfolios. Adviser makes no representations that any of the securities discussed have been or will be profitable. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio.