“Few challenges to the Federal Reserve independence have ever matched the drama of Dec. 5, 1965. Fed Chaiman William McChesney Martin Jr. had just convinced the Board of Governors to raise the discount rate amid signs that the economy was starting to overheat.”

~ The Federal Reserve Bank of Richmond—1965: The Year the Fed and LBJ Clashed

“Summoned then-Fed Chairman William McChesney Martin to Johnson’s Texas Ranch where Johnson shoved him against the wall. Physically assaulting the Fed chairman is probably a greater threat to Federal Reserve independence than questioning the Fed’s policy on Twitter.”

~“When LBJ Assaulted a Fed Chairman", The Mises Wire, 7/31/2018

“With fewer than 11 months until the election and four days until the next meeting of the Federal Open Market Committee, Burns and Nixon held a private telephone conversation. Burns states that: ‘I wanted you to know that we lowered the discount rate; got it down to 4.5%.’ ‘ Good, good, good,’ replies Nixon.”

~“How Richard Nixon Pressured Arthur Burns: Evidence from the Nixon Tapes”, February 2006

Those inclined to view President Trump’s needling of Federal Reserve Chairman Jerome Powell as an unprecedented breach of decorum might wish to brush up on their monetary history. The truth is, tormenting the Fed chairman—whether through verbal assault, political manipulation, or, on at least one remarkable occasion, an actual shove—has long been part of the American political tradition. Over the past sixty years, this peculiar sport has produced no shortage of high drama and, more worryingly, some truly calamitous inflation.

The pressures now bearing down on Jerome Powell have an air of déjà vu about them—eerily so. If whispers from the Hill Country are to be believed, the last time a Fed Chairman found himself in similar crosshairs, it ended with a shove against the stone wall of a Texas ranch house, courtesy of President Lyndon B. Johnson himself. That chairman was William McChesney Martin. Not long after, another president—Richard Nixon—took a more insidious, if less physical, approach, orchestrating a sustained campaign of psychological siege against Arthur Burns between 1970 and 1972. In each case, the reason for the presidential ire was the same: interest rates were too high for political comfort. That same tension, dressed in the garments of a different era, now encircles Chairman Powell.

William McChesney Martin, with fifteen years at the helm of the Federal Reserve, had come to embody the very notion of postwar monetary statesmanship—a man who took central banking as seriously as a judge takes the law. Arthur Burns, for his part, was the very image of the learned economist: pipe in hand, gold standard in heart, and an unswerving belief that monetary policy should be both principled and apolitical. Yet when push came—quite literally, in Martin’s case—and presidential will collided with economic orthodoxy, both men yielded. Each, under the weight of executive pressure, sanctioned sweeping and ill-timed expansions of monetary policy. Their concessions helped ignite the runaway inflation of the 1970s. Natural resource equities were one of the few places to protect your portfolio. And now, half a century later, the same winds appear to be gathering once again.

Just as Martin and Burns, despite their reputations and resolve, eventually bowed to the pressure from their respective Commanders-in-Chief, we believe Jerome Powell will—sooner or later—do the same. Whether by reluctantly guiding interest rates downward himself or by exiting stage left to make room for a more compliant successor, the outcome is likely to be identical. One way or another, monetary policy will loosen. We are confident that Trump’s new appointee will arrive in his office; sleeves rolled up and rate cuts ready.

In both 1966 and 1971, monetary policy took a conspicuous turn toward accommodation—not because the economic data demanded it, but because the men in the Oval Office did. Faced with mounting inflationary pressures, the Fed, under Martin and later Burns, relented. The result? Inflation took off like a shot. Equities struggled and natural resource stocks were one of the only bright spots in the market. It is our firm belief that Jerome Powell stands at the same fateful crossroads. And if history is any guide—as it so often is—the road ahead leads not to price stability, but to another inflationary surge, just as potent as those that came before.

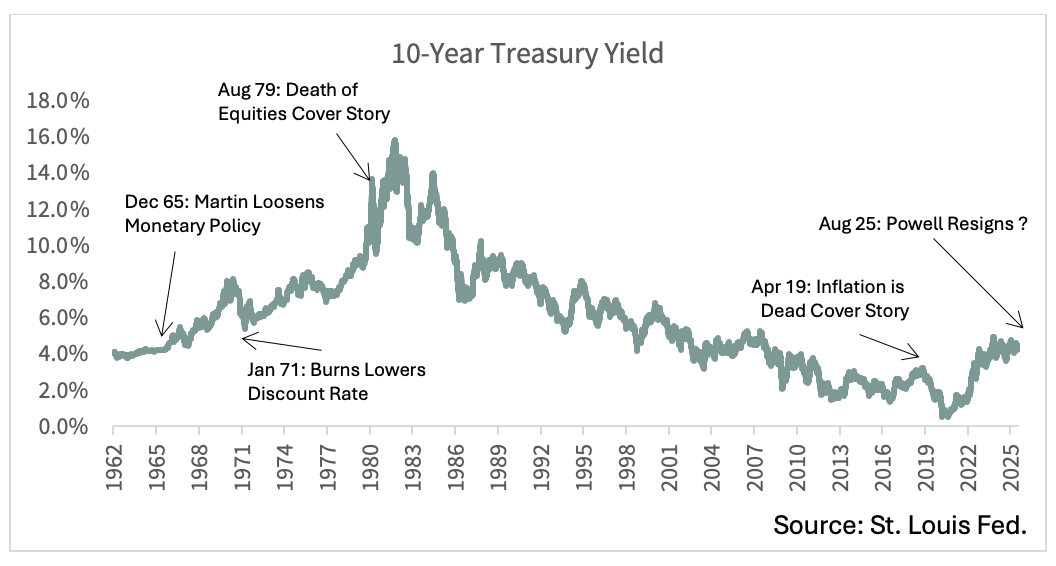

Since the close of the Second World War, the economic history of the United States can be read as a tale of two great arcs. First came the long, grinding rise of inflation—from the late 1940s through the early 1980s—a period in which prices climbed, yields soared, and policymakers seemed forever one step behind. Then, just as suddenly, came the great disinflation. Beginning in the early 1980s, it carried on—relentless, reassuring—until 2020. A glance at the yield on the 10-year U.S. Treasury bond over those seventy years tells the story better than any textbook: the rise, the fall, the quiet before the next storm.

We are firmly in the camp that believes the great disinflationary arc, which began in the stern days of Paul Volcker’s Fed, has run its course. The era of falling yields and fading price pressures is over. In its place, a new cycle has begun—an inflationary one, with the potential to stretch across decades. And if history is any indication, it will not pass quietly. It will bring with it the kind of problems that compound—politically, economically, and socially—until they can no longer be ignored.

In the spring of 2019, we issued a quiet but pointed warning to our investors: prepare for the return of inflation. That same month, Bloomberg Businessweek proclaimed exactly the opposite. With triumphant finality, their April cover declared “Is Inflation Dead?”—a eulogy of sorts to the seventy-year war against rising prices. As if to underscore the verdict, they paired the headline with a fallen dinosaur, belly-up and extinct, as though inflation had gone the way of the brontosaurus. It was, in our view, a cover destined for the contrarian’s scrapbook.

In response, we penned a piece of our own—“The Bell Has Been Rung: The Contrarian Power of Magazine Covers”—and made a rather unorthodox prediction. We suggested that Businessweek’s dinosaur-clad proclamation would prove as clairvoyant in calling the return of inflation as its infamous August 1979 cover, “The Death of Equities,” had been in heralding the greatest stock market boom in American history. As far as contrarian indicators go, magazine covers have a way of getting the direction right—just not in the way their editors intend.

That 1979 Businessweek cover, mournfully announcing “The Death of Equities,” turned out to be less an obituary than a starting gun. To the attentive—and there were few—it signaled that inflation was near its apex, that equities were historically cheap, and that a secular bull market was preparing to stir. Most investors, of course, ignored the message entirely. Warren Buffett was not among them. The market didn’t roar back overnight; in fact, it slumbered for three more years. But come August 1982, it awoke with a vengeance—and from that moment, the surging market has not looked back.

History, never one to pass up an encore, staged a familiar act. Nearly two years after Businessweek’s “End of Inflation” pronouncement, the beast returned. By the summer of 2021, inflation—stoked by the chaos of pandemic-era supply chains—had clawed its way back to nearly 6%. A year later, it breached 9%, territory unseen since disco and stagflation shared the headlines. And just as the equity bull market that began in 1982 grew more speculative with age, we believe this inflationary cycle is likewise just getting warmed up. The 2021–2022 surge was the overture; the real crescendo, we fear, still lies ahead. We believe that just like in the 1970s, natural resource equities will become crucial to protect a portfolio’s purchasing power.

Investors, ever eager to believe in happy endings, have largely declared the inflation scare of 2021 a closed chapter. The narrative now making the rounds is one of restored order—of price stability returning like an old friend, ready to stay a while. The exuberant rebound in long-duration assets, especially the ever-popular large-cap growth stocks, has only added fuel to this comforting belief. If the markets are a mood ring, they are glowing with complacency.

But markets, like parties, have a way of ending just when the dancing gets good. In our view, the crowd is misreading the signs. Beneath the surface calm lies something far more combustible. The renewed political pressure bearing down on the Federal Reserve—quiet to some, unmistakable to others—carries with it deeply unsettling implications. We believe inflation is not retreating, but merely pausing. And soon enough, it will accelerate again—swiftly, stubbornly, and disruptively.

William McChesney Martin, who presided over the Federal Reserve from 1951 to 1970, is best remembered for a metaphor that has aged better than most monetary theories: the job of the Fed, he said, was to take away the punch bowl just as the party gets going. In December of 1965, Martin decided it was time to make good on that credo. With the U.S. economy running a fever—fueled by the twin furnaces of Vietnam War spending and the domestic ambitions of the Great Society—he nudged the discount rate up by 50 basis points. It was, in his view, time to signal last call.

President Lyndon B. Johnson, on the other hand, had little patience for teetotalers at his party. While Martin fussed with the punch bowl, Johnson wanted to keep it flowing—generously and without interruption. With an escalating war in Southeast Asia and an ambitious domestic agenda at home, the President needed low interest rates like a patient needs oxygen. Martin believed rates had to rise. Johnson insisted they must fall. In such moments, compromise tends to give way to confrontation.

So it was that Martin found himself summoned, like an unruly subordinate, to President Johnson’s ranch in December 1965. What unfolded there now lives in central banking lore. According to those present, the encounter was less a meeting than a mauling. Johnson, never known for subtlety, let loose with a torrent of invective—waving his arms, crowding Martin’s space, and, if accounts are to be believed, even shoving him against the wall. The message was unmistakable: the discount rate hike must be undone. Martin, to his credit, stood firm. This only further enraged Johnson, who saw Martin’s resistance not merely as insubordination but as a constitutional affront. “You went ahead and did something that I disapprove of,” the President barked. “It will affect my entire term here.” Then came the line that echoed across history: “My boys are dying in Vietnam, and you won’t print the money I need.”

Though visibly rattled by his Lyndonland encounter, Martin did not give Johnson the immediate trophy he sought. The discount rate remained untouched—for a time. Yet in the months that followed, the Fed under Martin’s stewardship began to soften its stance. Reserve requirements were eased. Open-market operations took a more generous turn. The money supply, like champagne at a state dinner, began to flow more freely. And then, in May of 1967—perhaps as a gesture to a still-undecided Johnson—Martin quietly trimmed the discount rate by 50 basis points, bringing it back to 4.0%. The principle may have remained, but the posture had changed.

In hindsight—a lens that spares no one—Martin’s pivot toward easier money proved to be a grievous error. When he first stood his ground in late 1965, inflation hovered at a modest 2.4%. By the close of the decade, it had vaulted past 6%. While Arthur Burns would later inherit—and amplify—the inflationary mess, the seeds had already been sown. Today, many economists argue that the great inflation of the 1970s did not begin with Burns at all, but rather with Martin, whose reluctant concessions marked the true turning point. The blame, it seems, lies less with the man who poured the gasoline than with the one who struck the match.

The Federal Reserve Bank of Richmond, never one for drama, nonetheless titled its retrospective: “1965: The Year the Fed and LBJ Clashed.” Within its pages lies a scholarly consensus that has grown only firmer with time—that the true origins of the 1970s inflationary spiral trace back to the 1960s. Economic historian Allan Meltzer called 1965 the pivotal year, the moment the dam began to crack. Robert Hetzel, chronicling the Fed’s internal history, pointed squarely at Martin’s role: any explanation of the Great Inflation, he wrote, must come to terms with Martin’s responsibility. It was a judgment Martin himself appeared to accept. At his 1970 retirement party, in a moment of rare candor for a central banker, he looked around the room and simply said, “I’ve failed.”

Anyone hoping that the Martin–Johnson saga was a one-off—an unfortunate but isolated rupture in the normally decorous relationship between President and Fed—was soon disabused of the notion. The era of open confrontation between the White House and Constitution Avenue was only just beginning.

When Richard Nixon won the presidency in 1968, he did not wait long to settle old scores. By 1970, with William McChesney Martin stepping down, Nixon seized the opportunity to appoint a Federal Reserve Chairman of his own choosing—and of his own memory. The man he selected, Arthur Burns, was not only a respected economist but an old confidant from the Eisenhower years, during which Burns had chaired the Council of Economic Advisors and cultivated a close rapport with then–Vice President Nixon. It had been Burns, back in 1958 and 1959, who warned Nixon that interest rates were politically perilous—that if the Fed didn’t lower them from 4% to 2%, the Republican Party would pay the price. Nixon believed him, and when he narrowly lost the 1960 election, he pinned the blame not on Kennedy’s charisma but on Martin’s monetary restraint. A decade later, Nixon wasn’t about to let history repeat itself. Burns was the perfect candidate—not just for his résumé, but because he had once told Nixon exactly what Nixon had always wanted to hear.

And Nixon, true to form, was not about to let Arthur Burns forget the script. No sooner had Burns taken the chairmanship in 1970 than the pressure campaign began. The next election was still two years off, but Nixon was already pacing the map like a candidate in the final stretch. He wanted rates down—aggressively, visibly, unmistakably down. Burns, at least in public, resisted. He spoke of inflationary risks, of monetary discipline, of the Fed’s independence. But the man in the Oval Office had other ideas, and he wasn’t known for taking no as a final answer.

For the next eighteen months, Arthur Burns found himself in a slow, relentless squeeze. Nixon didn’t apply the pressure directly—at least not always. Instead, he deployed his operatives: the famously hard-edged John Ehrlichman, the ever-watchful H.R. Haldeman, and eventually, the swaggering new Treasury Secretary, John Connally. Their message was unambiguous and unrelenting: the President wanted lower rates, and he had little patience for academic lectures on central bank autonomy. Burns, who took great pride in his independence, was told—point-blank—that it was time to let go of such illusions. The President didn’t want a philosopher at the Fed. He wanted a team player.

For those with a taste for the darker corners of monetary history, Amity Shlaes’s Great Society: A New History is essential reading. In it, she chronicles with unsettling detail the campaign of pressure—verging on psychological warfare—that Nixon’s inner circle waged against Arthur Burns. The image is striking: Burns, the scholarly, pipe-smoking central banker, clinging to notions of independence, surrounded by a White House phalanx bent on submission. At the center of the final push stood Treasury Secretary John Connally—gruff, commanding, and politically shrewd—who delivered the kind of bare-knuckled persuasion Nixon prized. The campaign reached its bizarre crescendo in the summer of 1971, when The Wall Street Journal published a story claiming that Burns and Connally were discussing the outright absorption of the Federal Reserve into the Treasury, with Burns angling for a 50% pay raise in the process. None of it was true. The piece had been planted—by Connally, with Nixon’s blessing—for the sole purpose of humiliating Burns in public view. It was policy by ambush.

In the end, Arthur Burns capitulated. After months of siege from Pennsylvania Avenue, the Fed Chairman laid down his arms. The discount rate, once held at 6%, was trimmed to 4.5% by the summer of 1972. The results were as swift as they were dramatic. Between late 1970 and the end of 1972, the money supply ballooned—both M1 and M2 grew by 50%—and unemployment figures began to edge downward. Nixon, who had vowed there would be no repeat of 1960, got exactly what he wanted: a turbocharged economy and, come November, a landslide reelection. Burns had delivered—and history would judge the cost later.

Nixon, of course, was jubilant—this was before Watergate began its slow-motion detonation—but the U.S. economy was walking straight into a minefield. Easy money, so politically expedient in the short term, was about to collide with something far more destabilizing: the collapse of the postwar monetary order. In the summer of 1971, the U.S. officially severed the dollar’s link to gold, dismantling the Bretton Woods framework. The result was swift and severe. The dollar, in terms of gold, plunged. Inflation, which had been hovering at a relatively tame 2.7%, surged past 7% within a year. And when the Arab Oil Embargo hit in September 1973, the inflation rate didn’t just rise—it detonated, pushing well beyond 12%. The reckoning had arrived.

Looking back, it’s clear that Arthur Burns’s policies—however reluctantly enacted, and however much they strained against his own economic instincts—ended in calamity. The inflation that followed was not a byproduct of unforeseeable shocks, but the direct result of decisions made under pressure. As Burton Abrams observed in his forensic essay, How Richard Nixon Pressured Arthur Burns: Evidence from the Nixon Tapes, it’s difficult to make sense of the Fed’s 1972 monetary largesse without acknowledging the White House’s hand. “It is hard to explain,” Abrams writes, “how a man of Arthur Burns’s experience, intellect and political know-how could be pressured into abandoning his better judgment.” And yet he was. Whatever the mix of motives—fear, loyalty, political arithmetic—Burns’s actions helped unleash one of the most punishing inflationary episodes in American economic history.

The strain now being applied to Jerome Powell bears an uncomfortable resemblance to the pressure once exerted on Martin and Burns. The tools may be more modern—press conferences and social media rather than ranch house shoving matches or planted newspaper stories—but the intention is unmistakably familiar. If history is any guide, Powell will be faced with the same grim choice: accommodate the president’s wishes by cutting rates, or step aside in favor of someone more compliant. One way or another, the outcome looks poised to rhyme with the past.

In 1965, Lyndon Johnson needed cheap money to bankroll a two-front war—one in Vietnam, the other under the banner of the Great Society. In 1971, Richard Nixon needed an electoral landslide, and easier credit was the surest path to prosperity at the polls. Today, Donald Trump faces a different arithmetic: the staggering cost of servicing a national debt that dwarfs anything Johnson or Nixon ever contemplated. All three presidents had compelling reasons for wanting rates lower. Two succeeded—and the inflation that followed was swift, punishing, and historic. If Trump gets his way, as history strongly suggests he will, the inflationary fallout may once again be just as severe.

We believe the page has turned. A new, long inflationary cycle is now underway. Just as the infamous 1979 BusinessWeek cover inadvertently signaled the end of rising prices—and the moment to buy long-duration financial assets with both hands—the 2019 cover did the opposite. Its declaration that inflation was dead marked, in our view, the beginning of its resurrection. Back in ’79, few paid attention. It took three years before the true meaning of that cover became obvious—obvious, and immensely profitable. The 2019 warning has been similarly dismissed. Yet here we are: inflation is already back, and still the market clings to the fiction that it will quietly fade away.

Following the publication of that fateful 1979 BusinessWeek cover, inflation did indeed retreat—slowly at first, then with lasting force, for more than four decades. But cycles, like tides, return. We believe the inflationary era now beginning could match that disinflationary stretch in both length and consequence. And once again, the match may be struck at the Federal Reserve. Just as Martin and Burns—each under immense presidential pressure—reluctantly opened the monetary spigots, we suspect Jerome Powell will do the same. Whether by resignation or capitulation, the result will be familiar: a surge in inflation, swift and difficult to contain. The past, it seems, is not done with us yet.

Curious to explore more of our research on the Natural Resources market? Download our Q1 2025 research newsletter below.

Registration with the SEC should not be construed as an endorsement or an indicator of investment skill, acumen or experience. Investments in securities are not insured, protected or guaranteed and may result in loss of income and/or principal. Historical performance is not indicative of any specific investment or future results. Investment process, strategies, philosophies, portfolio composition and allocations, security selection criteria and other parameters are current as of the date indicated and are subject to change without prior notice. This communication is distributed for informational purposes, and it is not to be construed as an offer, solicitation, recommendation, or endorsement of any particular security, products, or services. Nothing in this communication is intended to be or should be construed as individualized investment advice. All content is of a general nature and solely for educational, informational and illustrative purposes. This communication may include opinions and forward-looking statements. All statements other than statements of historical fact are opinions and/or forward-looking statements (including words such as “believe,” “estimate,” “anticipate,” “may,” “will,” “should,” and “expect”). Although we believe that the beliefs and expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such beliefs and expectations will prove to be correct. Various factors could cause actual results or performance to differ materially from those discussed in such forward-looking statements. All expressions of opinion are subject to change. You are cautioned not to place undue reliance on these forward-looking statements. Any dated information is published as of its date only. Dated and forward-looking statements speak only as of the date on which they are made. We undertake no obligation to update publicly or revise any dated or forward-looking statements. Any references to outside data, opinions or content are listed for informational purposes only and have not been independently verified for accuracy by the Adviser. Third-party views, opinions or forecasts do not necessarily reflect those of the Adviser or its employees. Unless stated otherwise, any mention of specific securities or investments is for illustrative purposes only. Adviser’s clients may or may not hold the securities discussed in their portfolios. Adviser makes no representations that any of the securities discussed have been or will be profitable. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio.