The article below is an excerpt from our Q2 2024 commentary.

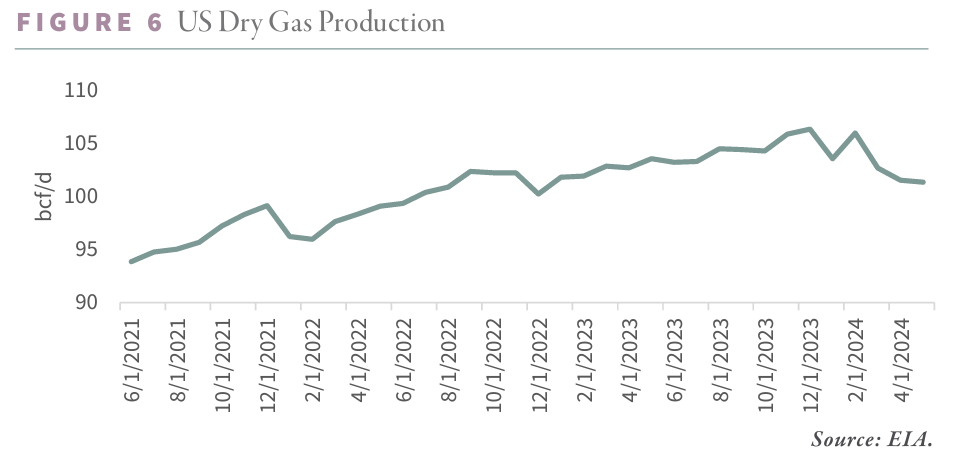

Natural gas production is plummeting—a condition noted by almost no analysts. Between December 2023 and May 2024, U.S. dry gas supply has contracted by a notable 5 billion cubic feet per day—a nearly 5% reduction. On a year-over-year basis, the decline stands at 2.2 bcf/d. The drawdown is the sharpest since the shale revolution began, excluding the 2020 COVID year. Both shale and conventional production have taken a hit, with shale output diminishing by 2.1 bcf/d and conventional sources plummeting by 2.8 bcf/d over the last five months.

In the history of shale production, the current year marks the first-ever non-COVID-related year-on-year decline, with the shales recording a reduction of 1.9 bcf/d as of May. The Marcellus, the once-mighty giant, has seen its production fall by 1.1 bcf/d since December, while the Haynesville has shed 500 mmcf/d. The Permian Basin still stands as the lone growth exception, eking out a modest gain of 265 mmcf/d over the same period.

The Permian’s resilient gas production, despite a concurrent decline in crude output, raises intriguing questions. The basin’s rising gas-oil ratio has been a topic of much debate, with some analysts pointing to it as evidence of maturation—a sort of geological canary in the coal mine. The theory suggests that as a basin depletes, field pressures decline, allowing more gas to escape from solution and rise up the well bore—a phenomenon akin to a soda can being opened. A petroleum engineer would say an increase in the gas-oil ratio is a signal that declines in a basin's oil production is rapidly approaching. Yet, we have long been skeptical of such prognostications. The Permian’s gas growth, we argued, was a simple matter of shifting rigs from the oil-rich Midland to the gas-heavy Delaware. But recent divergences between oil declines and gas growth warrants a reconsideration of our theory. Could it be that depletion is finally impacting the gas-oil ratio? If so, we should expect the Permian’s oil and gas output to both exhibit declines.

The recent downturn in U.S. gas production has been widely attributed to low prices. The Henry Hub benchmark has languished at $2.00 per mmcf throughout 2024—a level not seen in the last quarter-century except in the nadirs of 1999, 2016, and 2020 . In those years, oil prices were equally depressed, with WTI averaging $14, $27, and even plunging to -$47 per barrel during the pandemic. Today, WTI trades at $75 per barrel, yet natural gas, on an energy-equivalent basis, remains at an 84% discount—a discount reminiscent of the all-time low in 2012.

In our previous letters, we noted the dissimilarities between today’s gas market and that of 2012. Back then, shale production was poised to soar; today, it is in retreat. The U.S., once bereft of export capabilities, now stands as the world’s largest LNG supplier.

While low prices have certainly dampened drilling activity—evidenced by the gas-directed rig count, which has fallen to 100 rigs from 166 in 2022 and 200 in 2019—price alone does not tell the full story. We posit that the shale gas basins are simply running out of high-quality drilling inventory. Our proprietary neural network, developed in 2018 to analyze shale trends, has long indicated that the Marcellus, Haynesville, and Permian were approaching peak production. Now, all three basins have produced 50% of their total recoverable reserves, a harbinger of imminent declines. Particularly in the Marcellus and Haynesville, the depletion of Tier 1 drilling locations combined with falling rig counts strongly suggests that production declines should accelerate.

There is a parallel to be drawn here with the oil shales during the COVID-induced downturn. In late 2019, our neural network foresaw declines in the Bakken and Eagle Ford, with the Permian soon to follow. When oil prices collapsed, the rig count plummeted, and production followed suit. Many believed the declines would be temporary, rebounding as prices recovered. But as oil climbed past $50, $60, and even $70 per barrel, it became clear that geology, not economics, was the culprit. Apart from the Permian, none of the mature shale basins were able to regain their pre-COVID highs in drilling activity.

Now, our models suggest that every shale gas basin, including the associated gas from the Permian, mirrors the Bakken and Eagle Ford in 2019. Will history repeat itself? Will higher prices fail to reverse the underlying depletion and arrest the production decline? We believe the answer is yes.

During our Investor Day on October 21, 2024, we delved into the latest insights from our artificial intelligence models. A replay is available, click here.

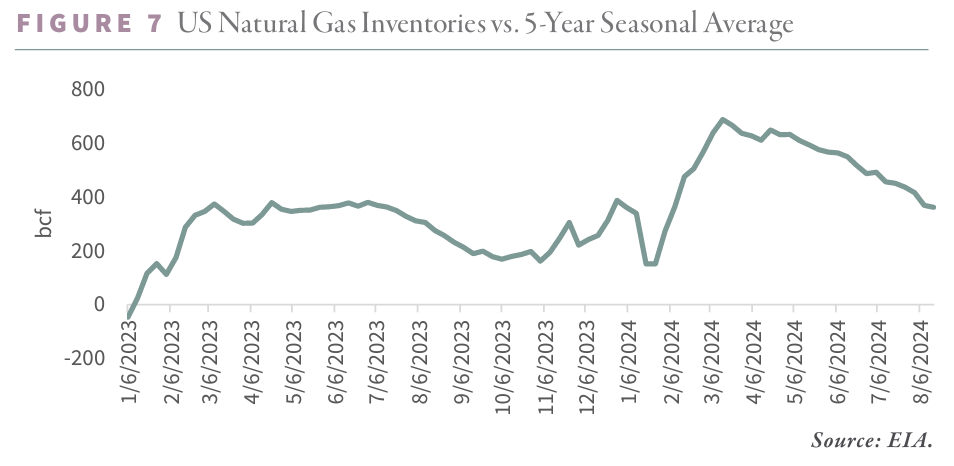

The U.S. natural gas market is now in the grip of a sharp and sustained deficit, as evidenced by inventory trends, which stands in contrast to the bearishness of investors. Following a mild winter, mid-March inventories stood nearly 700 bcf above the five-year seasonal average—a near record. Yet, in just five months, the surplus has been halved, now standing at 325 bcf.

Once in surplus by approximately 1 bcf/d, the U.S. gas market has swung into a deficit of over 2 bcf/d—one of the sharpest reversals on record. While a hotter-than-average summer contributed to this shift, our models attribute most of the change to collapsing production. When we last wrote, we expected inventories to end July 544 bcf above average; instead, they were only 435 bcf higher than normal. By mid-August, the surplus had eroded further to just 325 bcf.

Highlighting the tightening market, August 6th saw an inventory draw of 6 bcf/d—a modest number, but significant for occurring during the summer injection season. Since 1998 there have been only four summer withdrawals (out of 312 summer weeks). Two of these withdrawals occurred in the brutally hot summer of 2006, and two were hurricane-related.

Our previous forecast called for year-end inventories to be 360 bcf above average, turning into a deficit sometime in 2025. Yet, with inventories already below our bullish year-end forecast, we now expect the surplus to be completely eroded by year’s end—just as new LNG capacity begins to come online. The next two years will witness the fastest growth of LNG export capacity in U.S. history. Where the industry will source the gas remains an open question.

As new LNG terminals come online, setbacks and delays are inevitable. Indeed, the first such delay has already occurred. In the second quarter, the Golden Pass joint venture between Exxon and Qatar Energy announced a three-month delay in commissioning their first train after their EPC contractor, Zachry Holdings, declared bankruptcy. The first train, expected to consume 680 mmcf/d, was initially slated for March 2025 but is now expected in June, with subsequent trains following in December 2025 and March 2026.

While delays such as this postpone one source of new short-term demand, our medium-term outlook remains unchanged. U.S. natural gas trades at an 84% discount to its energy equivalent, making it the cheapest molecule of energy on the planet. Gas for delivery in Europe remains $12 per mcf, while Asian LNG fetches $13.50 per mcf, compared with $2.00 in the U.S. As new LNG demand comes online and production continues to disappoint, inventories will continue to tighten, pushing prices toward the global benchmark. We cannot recall a more asymmetric investment opportunity than U.S. natural gas.

Intrigued? We invite you to download or revisit our entire Q2 2024 research letter, available below.

Disclosures:

Registration with the SEC should not be construed as an endorsement or an indicator of investment skill, acumen or experience. Investments in securities are not insured, protected or guaranteed and may result in loss of income and/or principal. Historical performance is not indicative of any specific investment or future results. Investment process, strategies, philosophies, portfolio composition and allocations, security selection criteria and other parameters are current as of the date indicated and are subject to change without prior notice. This communication is distributed for informational purposes, and it is not to be construed as an offer, solicitation, recommendation, or endorsement of any particular security, products, or services. Nothing in this communication is intended to be or should be construed as individualized investment advice. All content is of a general nature and solely for educational, informational and illustrative purposes. This communication may include opinions and forward-looking statements. All statements other than statements of historical fact are opinions and/or forward-looking statements (including words such as “believe,” “estimate,” “anticipate,” “may,” “will,” “should,” and “expect”). Although we believe that the beliefs and expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such beliefs and expectations will prove to be correct. Various factors could cause actual results or performance to differ materially from those discussed in such forward-looking statements. All expressions of opinion are subject to change. You are cautioned not to place undue reliance on these forward-looking statements. Any dated information is published as of its date only. Dated and forward-looking statements speak only as of the date on which they are made. We undertake no obligation to update publicly or revise any dated or forward-looking statements. Any references to outside data, opinions or content are listed for informational purposes only and have not been independently verified for accuracy by the Adviser. Third-party views, opinions or forecasts do not necessarily reflect those of the Adviser or its employees. Unless stated otherwise, any mention of specific securities or investments is for illustrative purposes only. Adviser’s clients may or may not hold the securities discussed in their portfolios. Adviser makes no representations that any of the securities discussed have been or will be profitable. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio.